Statue of Liberty in front of the New York City skyline.

I wrote yesterday about the most recent OECD numbers on “Average Individual Consumption” in member nations.

There was a very clear lesson in that data about the dangers of excessive government. The United States was at the top in this measure of household living standards,

Indeed, the only countries even remotely close to the United States were oil-rich Norway and the two tax havens of Switzerland and Luxembourg.

Those AIC numbers gave us an interesting snapshot of relative living standards in 2014.

But what would we discover if we looked at how that data has changed over time?

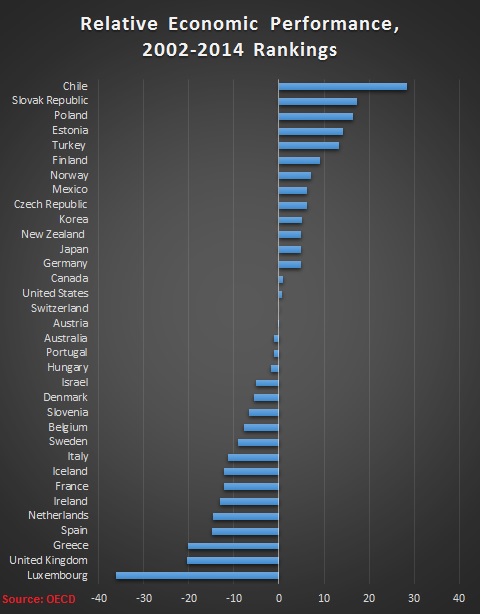

It appears that the OECD began assembling that data back in 2002. Here’s a table showing how nations rose or fell, relative to other OECD nations, since then. Based on convergence theory, one would expect to see that poorer nations enjoyed the biggest relative gains, while richer nations fell in the rankings. And that is what generally happened, but with some notable exceptions.

Here are the countries that did not conform, for either good reasons or bad reasons, to convergence theory.

We’ll start with the nations that have bragging rights.

Now for the nations that did not fare well.

If you like this kind of data on whether nations are trending in the right direction or wrong direction, I’ve also tinkered with the data from Economic Freedom of the World.

I also looked specifically at changes in Europe this century and did not find any reason for optimism.

The bottom line is that there’s no substitute for free markets and limited government. If nations want faster growth and more prosperity, they need to mimic jurisdictions such as Hong Kong and Singapore.

Unfortunately, there’s very little reason to be optimistic about that happening in Europe.

The most damning journalistic sin committed by the media during the era of Russia collusion…

The first ecological study finds mask mandates were not effective at slowing the spread of…

On "What Are the Odds?" Monday, Robert Barnes and Rich Baris note how big tech…

On "What Are the Odds?" Monday, Robert Barnes and Rich Baris discuss why America First…

Personal income fell $1,516.6 billion (7.1%) in February, roughly the consensus forecast, while consumer spending…

Research finds those previously infected by or vaccinated against SARS-CoV-2 are not at risk of…

This website uses cookies.