A Win By Any Measure on Wall Street Monday Amid Trade Fears

Markets concept depicting the American flag draped over the New York Stock Exchange (NYSE) at Wall Street. (Photo: AdobeStock)

By any measure, stocks staged an impressive recovery late Monday, as what began as roughly 2% losses across the board were dramatically reduced by the closing bell.

Market internals continue to impress. The final adv/decl stats settled with 3 stocks advancing for every 4 declining at both the New York Stock Exchange (NYSE) and the NASDAQ Composite (^IXIC) marketplace. While still slightly negative, this was much improved from most of the day, and a sign of market resilience.

The Russell 2000 (^RUT) outperformed for the third consecutive session as it eked out the smallest of gains at +0.95, or +0.1% to 1614.98. The Russell was the only broad market Average to close in the green. It’s an endorsement from investors and signals small caps will benefit from strong economic growth, while remaining isolated from the strength of the U.S. dollar and most trade issues.

The Dow Jones Industrial Average (^DJI) ended the day with a decline of 66 points, or merely -0.3% to 26438. This was much improved from starting the day with nearly a 500 point deficit, or -1.8%. While many megs cap multinationals in the (^DJI) are very sensitive to trade issues, Walt Disney Co. (DIS), Chevron Corporation (CVX), UnitedHealth Group Inc (UNH), and McDonald’s Corp (MCD) all settled with solid gains.

Both the S&P 500 (^SPX) and NASDAQ Composite (^IXIC) finished with losses of just less than -0.5%, again much improved from their early morning declines.

The (^SPX) was aided by a positive reversal in oil prices during the day that gave support to the energy sector. Additionally, Occidental Petroleum Corporation (OXY) raising the cash portion of their bid to acquire Anadarko Petroleum Corporation (APC) helped valuations among E&P names, many of which are upper tier components of the S&P 500.

The (^IXIC) was the arguably the most challenged to reverse fortunes on the day. Not only did it begin the day with the largest decline at -2.2% but it’s also the trading home to countless technology companies. That includes the entire semiconductor space, which are highly exposed to the pan Asian economy.

No doubt investors will pay close attention to markets in China overnight. Although in Shanghai the SSE Composite Index (^SSE) declined -5.5% Monday, it still has YTD gains of greater than +20%. Further market declines in China overnight during Tuesday trading could set the stage for another challenging trading day in the U.S. on Tuesday.

Graphic concept for U.S.-China trade war, tariffs on imports and exports. (Photo: AdobeStock)

Stocks ended a two-day slide on Friday as investors responded with optimism to the Employment Situation in April that included much stronger jobs gains than expected, solid earnings growth, and the lowest unemployment rate in 49 years.

With the backdrop of remarkably low inflation from PCE data earlier in the week, the April gains in non-farm payrolls of +263,000, versus a consensus of +180,000 was a strong confirmation. The ADP National Employment Report released two days earlier found private sector payrolls were +275,000, beating the consensus by +100,000. It was the first month this year that both reports posted a surprise in upside results.

The rally was broad based and without hesitation.

The S&P 500 (^SPX) gained +1% to close a fraction from it’s all time high set just 3 days earlier. As a testament to the breadth of the rally, all 11 sectors of the S&P closed with gains.

The NASDAQ Composite (^IXIC) rallied +1.6%, just enough to post a new closing high of 8164.00, a few points better than its prior high from the previous Thursday. The NASDAQ now has a string of six consecutive weekly gains.

The Dow Jones Industrial Average (^DJI) gained +0.75% to 2650.95. The Dow slightly underperformed for the week after a few high profile earnings misses and remains -1.2% from its ATH of 26828 from last September.

Positive Market Breadth Lifts Russell 2000 to 7-Month highs

The Russell 2000 (^RUT) was the standout performer of the day, rallying +2% to close at 1614.02, its highest close in 7 months.

This highlighted the positive breadth of Fridays rally. The Russell had also posted a gain of +0.4% Thursday, while the three larger capitalization indices all settled with modest declines, though well off their lows of the day. The Russell 2000 remains slightly more than -7% from its ATH of 1740 from late August last year.

While it has trailed the other indices, it has a history of rallying into the annual reconstitution in late June.

Market internals Friday were the best we’ve seen in over 10 weeks, consistent with the strength in the small caps shown by the Russell 2000.

At the NYSE advancing issues led decliners by nearly 3½ to 1. Among NASDAQ stocks it was a bit stronger at close to 4 to 1. We’ll be watching market breadth closely as a barometer on whether the market rally is broadening out.

Trade Tremors threaten Market Momentum

Investors fortitude will be challenged right out of the gate this week as trade negotiations between the U.S. and China are at a critical inflection point.

This was in bold print late Sunday following a warning by President Donald Trump of heightened tariffs on all Chinese goods by Friday in the absence of significant progress in the trade talks. The Chinese initial response was to suggest they may cancel the next round of talks scheduled for mid week.

The market reaction was decidedly negative with the Shanghai Composite declining -5.5% and early trading in U.S. equity futures pricing in an a lower opening of ~2%.

Since heightened trade tensions became a market focus just over a year ago, Equity Markets have shown a history of recovering quite well from selloffs sparked by negative headlines on trade.

Currently, the stakes may be higher as markets have continually priced in a higher probability of a favorable outcome. Should there be a hiatus in trade negotiations between the U.S. and China, a downside reaction may last longer than in the past.

Donald Trump is an incoherent mix of good policies and bad policies. Some of his potential 2020 opponents, by contrast, are coherent but crazy.

And economic craziness exists in other nations as well.

In a column for the New York Times, Jochen Bittner writes about how a rising star of Germany’s Social Democrat Party wants the type of socialism that made the former East Germany an economic failure.

Socialism, the idea that workers’ needs are best met by the collectivization of the means of production… A system in which factories, banks and even housing were nationalized required a planned economy, as a substitute for capitalist competition. Central planning, however, proved unable to meet people’s individual demands… Eventually, the entire system collapsed; as it did everywhere else, socialism in Germany failed. Which is why it is strange, in 2019, to see socialism coming back into German mainstream politics.

But this real-world evidence doesn’t matter for some Germans.

Kevin Kühnert, the leader of the Social Democrats’ youth organization and one of his party’s most promising young talents, has made it his calling card. Forget the wannabe socialism of American Democrats like Bernie Sanders or Alexandria Ocasio-Cortez. The 29-year-old Mr. Kühnert is aiming for the real thing. Socialism, he says, means democratic control over the economy. He wants to replace capitalism… German neo-socialism is profoundly different from capitalism. …Mr. Kühnert took specific aim at the American dream as a model for individual achievement. …“Without collectivization of one form or another it is unthinkable to overcome capitalism,” he told us.

What makes Kühnert’s view so absurd is that he obviously knows nothing about his nation’s history.

Just in case he reads this, let’s look at the evidence.

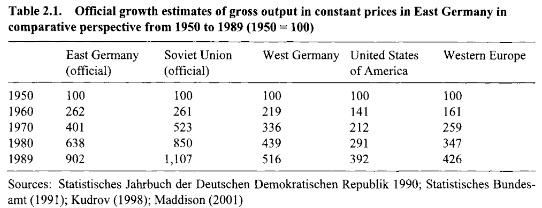

Jaap Sleifer’s book, Planning Ahead and Falling Behind, points out that the eastern part of Germany was actually richer than the western part prior to World War II.

The entire country’s economy was then destroyed by the war.

What happened afterwards, though, shows the difference between socialism and free enterprise.

Before…the Third Reich the East German economy had…per capita national income…103 percent of West Germany, compared to a mere 31 percent in 1991. …Here is the case of an economy that was relatively wealthy, but lost out in a relatively short time… Based on the official statistics on national product the East German growth rates were very impressive. However, …the actual performance was not that impressive at all.

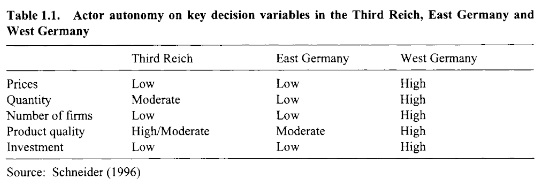

Sleifer has two tables that are worth sharing.

First, nobody should be surprised to discover that communist authorities released garbage numbers that ostensibly showed faster growth.

What’s really depressing is that there were more than a few gullible Americans – including some economists – who blindly believe this nonsensical data.

Second, I like this table because it confirms that Nazism and communism are very similar from an economic perspective.

Though I guess we should give Germans credit for doing a decent job on product quality under both strains of socialism.

For those who want to read further about East German economic performance, you can find other scholarly articles here, here, and here.

I want to call special attention, though, to a column by an economist from India. Written back in 1960, even before there was a Berlin Wall, he compared the two halves of the city.

Here’s the situation in the capitalist part.

The contrast between the two Berlins cannot miss the attention of a school child. West Berlin, though an island within East Germany, is an integral part of West German economy and shares the latter’s prosperity. Destruction through bombing was impartial to the two parts of the city. Rebuilding is virtually complete in West Berlin. …The main thoroughfares of West Berlin are near jammed with prosperous looking automobile traffic, the German make of cars, big and small, being much in evidence. …The departmental stores in West Berlin are cramming with wearing apparel, other personal effects and a multiplicity of household equipment, temptingly displayed.

Here’s what he saw in the communist part.

…In East Berlin a good part of the destruction still remains; twisted iron, broken walls and heaped up rubble are common enough sights. The new structures, especially the pre-fabricated workers’ tenements, look drab. …automobiles, generally old and small cars, are in much smaller numbers than in West Berlin. …shops in East Berlin exhibit cheap articles in indifferent wrappers or containers and the prices for comparable items, despite the poor quality, are noticeably higher than in West Berlin. …Visiting East Berlin gives the impression of visiting a prison camp.

The lessons, he explained, should be quite obvious.

…the contrast of the two Berlins…the main explanation lies in the divergent political systems. The people being the same, there is no difference in talent, technological skill and aspirations of the residents of the two parts of the city. In West Berlin efforts are spontaneous and self-directed by free men, under the urge to go ahead. In East Berlin effort is centrally directed by Communist planners… The contrast in prosperity is convincing proof of the superiority of the forces of freedom over centralised planning.

Back in 2011, I shared a video highlighting the role of Ludwig Erhard in freeing the West German economy. Given today’s topic here’s an encore presentation.

Samuel Gregg, writing for FEE, elaborates about the market-driven causes of the post-war German economic miracle.

It wasn’t just Ludwig Erhard.

Seventy years ago this month, a small group of economists and legal scholars helped bring about what’s now widely known as the Wirtschaftswunder, the “German economic miracle.” Even among many Germans, names like Walter Eucken, Wilhelm Röpke, and Franz Böhm are unfamiliar today. But it’s largely thanks to their relentless advocacy of market liberalization in 1948 that what was then West Germany escaped an economic abyss… It was a rare instance of free-market intellectuals’ playing a decisive role in liberating an economy from decades of interventionist and collectivist policies.

As was mentioned in the video, the American occupiers were not on the right side.

Indeed, they exacerbated West Germany’s economic problems.

…reform was going to be easy: in 1945, few Germans were amenable to the free market. The Social Democratic Party emerged from the catacombs wanting more top-down economic planning, not less. …Further complicating matters was the fact that the military authorities in the Western-occupied zones in Germany, with many Keynesians in their contingent, admired the economic policies of Clement Atlee’s Labour government in Britain. Indeed, between 1945 and 1947, the Allied administrators left largely in place the partly collectivized, state-oriented economy put in place by the defeated Nazis. This included price-controls, widespread rationing… The result was widespread food shortages and soaring malnutrition levels.

But at least there was a happy ending.

Erhard’s June 1948 reforms…abolition of price-controls and the replacement of the Nazi-era Reichsmark with much smaller quantities of a new currency: the Deutsche Mark. These measures effectively killed off…inflation… Within six months, industrial production had increased by an incredible 50 percent. Real incomes started growing.

I’ll close with my modest contribution to the debate. Based on data from the OECD, here’s a look at comparative economic output in East Germany and West Germany.

West Germany versus East Germany, Per Capita Gross Domestic Product (GDP). (Source: Organization for Economic Co-operation and Development)

You’ll notice that I added some dotted lines to illustrate that both nations presumably started at the same very low level after WWII ended.

I’ll also assert that the blue line probably exaggerates East German economic output. If you doubt that claim, check out this 1990 story from the New York Times.

The bottom line is that the economic conditions in West Germany and East Germany diverged dramatically because one had good policy (West Germany routinely scored in the top 10 for economic liberty between 1950 and 1975) and one suffered from socialism.

These numbers should be very compelling since traditional economic theory holds that incomes in countries should converge. In the real world, however, that only happens if governments don’t create too many obstacles to prosperity.

American flag and U.S. dollar financial and economy concept. (Photo: AdobeStock)

The Labor Department (DOL) via the Bureau of Labor Statistics (BLS) reported Friday that wage growth exceeded 3% for the ninth straight month in April.

Wages, or average hourly earnings (AHE) for all employees on private nonfarm payrolls, rose by 6 cents to $27.77. Average hourly earnings of private-sector production and nonsupervisory employees increased by 7 cents to $23.31 in April.

Over the year, average hourly earnings have increased by 3.2%, making April the ninth straight month of wage gains above 3%.

“America’s workforce continues to see their paychecks grow, with year-over-year wage growth reaching 3.2%,” Secretary of Labor Alexander Acosta said following the release of the Employment Situation. “The year-over-year average hourly earnings have grown at or exceeded 3.0% for nine straight months.”

“Wage growth has not risen this fast since 2009.”

Indeed, wages saw the largest gain since the third quarter (Q3) 2008 during Q4 2018. In April, wage growth was sustained by upward pressure from historically strong labor demand and the unemployment rate fell to a 49-year low at 3.6%. Hispanic unemployment fell to an all-time record low at 4.2%.

“Both adult men and adult women saw declines in their unemployment rate with adult men at 3.4% and adult women at 3.1%, which was the lowest rate for adult women since 1953,” Secretary Acosta added in a statement.

“We continue our work toward increasing labor force participation and this month’s report further underscores the importance of the administration’s efforts expanding skills training so that more Americans can find family-sustaining career opportunities.”

The labor force participation rate ticked down 0.2% to 62.8% in April, essentially unchanged from a year earlier after a slight tick-up for the first time in years. The less cited but arguably more important employment-population ratio was unchanged at 60.6% in April. It has been either 60.6% or 60.7% since October 2018.

Series with themes reflecting a certain billionaire politician who won the 2016 presidential election touting a very strong labor market. (Photo: AdobeStock)

Total nonfarm payrolls rose by a strong 263,000 in April, and the unemployment rate fell to 3.6%, both easily beating the consensus forecast. Wages continued to rise and unemployment for Hispanic unemployment fell to a new all-time low.

Prior

Consensus Forecast

Forecast Range

Actual

Nonfarm Payrolls – M/M ∆

196,000

180,000

160,000 — 240,000

263,000

Unemployment Rate – ∆

3.8%

3.8%

3.7% — 3.8%

3.6%

Private Payrolls – M/M ∆

182,000

178,000

160,000 — 216,000

236,000

Manufacturing Payrolls – M/M ∆

-6,000

10,000

-6,000 — 20,000

4,000

Participation Rate

63.0 %

63.0%

62.9 % — 63.0%

62.8%

Average Hourly Earnings – M/M ∆

0.1 %

0.2%

0.1% — 0.4%

0.2%

Average Hourly Earnings – Y/Y ∆

3.2 %

3.3%

3.2% — 3.5%

3.2%

Avg Workweek – All Employees

34.5 hrs

34.5 hrs

34.5 hrs — 34.5 hrs

34.4 hrs

Construction added 33,000 jobs in April, fueled largely by nonresidential specialty trade contractors (+22,000). Heavy and civil engineering construction contributed 10,000. Construction has added 256,000 jobs over the past 12 months.

Manufacturing rose by 4,000 in April, a slight change for the third straight month. In the 12 months prior to February, the industry had added an average of 22,000 jobs per month.

“This report is very consistent with the March ADP report,” Tim Anderson, analyst at TJM Investments said. “It also break the string of what was 4 months of a ‘back-and-forth’ between jobs reports from BLS and ADP having conflicting or inconsistent results.”

On Wednesday, the ADP National Employment Report reported the U.S. private sector created 275,000 jobs in April, crushing the consensus forecast and range. The total number of jobs added in March was revised up from 129,000 to 151,000.

“If there is 1 disappointing item in the report, it is that the labor participation rate declined to 62.8% after holding 63.0 or better for the last 4 months,” Mr. Anderson added. “That is a longterm structural issue that still needs some work down the road.”

The Labor Department said labor force participation rate ticked down 0.2% to 62.8% in April, essentially unchanged from a year earlier after a slight tick-up for the first time in years.

The less cited but arguably more important employment-population ratio was unchanged at 60.6% in April. It has been either 60.6% or 60.7% since October 2018.

Wages, or average hourly earnings (AHE) for all employees on private nonfarm payrolls, rose by 6 cents to $27.77. Average hourly earnings of private-sector production and nonsupervisory employees increased by 7 cents to $23.31 in April.

Over the year, average hourly earnings have increased by 3.2%, making April the ninth straight month of wage gains above 3%.

The total number of jobs for February was revised up from +33,000 to +56,000, and March was revised down from +196,000 to +189,000. Combined for the two months, job creation was 16,000 stronger than previously reported.

Un mur de propagande, or a propaganda wall, promoting socialism behind Senator Bernie Sanders, D-I, Vt., left, and Alexandria Ocasio-Cortez, D-N.Y., right.

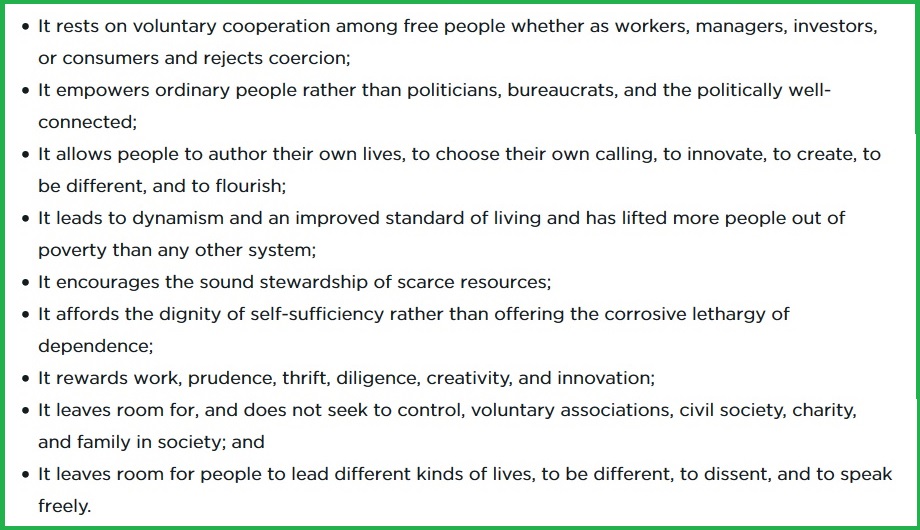

Since I think comparative economics can be very enlightening, I’m quite pleased to see a new study by David Burton of the Heritage Foundation, which uses several metrics to assess the relative merits of socialism and free enterprise.

This is not necessarily an easy task since socialism is a moving target.

Some people still adhere to the technical definition, which means government ownership, central planning, and price controls. While others assume that socialism is high tax rates and lots of redistribution.

Here’s David’s summary.

State ownership of the means of production is the central tenet of traditional socialist or communist thought. Traditional socialist and communist economic policies involve state-owned enterprises and a high degree of state control over all aspects of economic life. Over time, politicians came to understand that they did not need to have legal ownership of, or legal title to, businesses or other property in order to control them by regulation, administrative actions, or taxation. Furthermore, not having legal title meant that they could disclaim responsibility when government control did not work out well. Thus, the meaning of the term “socialist” evolved considerably during the last half of the 20th century to mean a strong state role in the economy, the pursuit of aggressive redistributionist policies, high levels of taxation and regulation, and a large welfare state—but not necessarily government ownership of the means of production.Regardless of how it’s defined, it doesn’t work. And the closer a country is to technical socialism, the greater the economic misery.

David reviews and analyzes a lot of material and I recommend the entire report.

For today’s purposes, though, I want to focus on his ethical arguments.

Here’s how he describes the morality of capitalism.

As a libertarian, I’m especially sympathetic to the argument about cooperative exchange versus coercion.

And I hope everyone agrees with the arguments about individual choice and civil society.

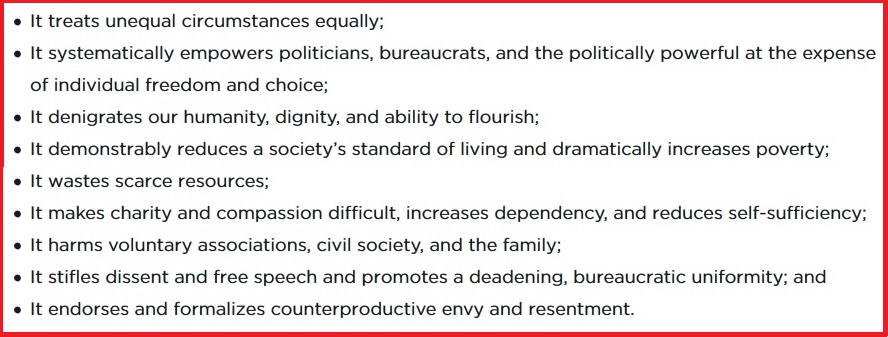

Now let’s look at David’s description of the morality of socialism.

For what it’s worth, I think the final point is the most compelling.

Socialism (whether the technical version or the redistribution version) basically creates a zero-sum game in which people are told it is moral to take from others simply because they produce more.

And this doesn’t necessarily mean the poor taking from the rich. Yes, that’s a big part of it, but there are all sorts of government programs that burden lower-income and middle-class people in order to line the pockets of the well-connected.

New York Stock Exchange (NYSE) Building in the Lower Manhattan Financial District, New York City. (Photo: Tomasz Zajda/AdobeStock/PPD)

We may be in the middle of a full-throttled firehose of earnings reports, but it’s still worth noting that Tuesday was the last day of the month. Any which way you slice it, the metrics of stock market performance in April were very acceptable, and that may even be an understatement when stacked on to Q1 performance.

Let’s take a closer look.

The Dow Jones Industrial Average (^DJI) at 26593 gained +2.5% in April and is +15.3% YTD. We can’t overstate how impressive for the ^DJI to post a gain in April, despite the number and severity of single-stock declines. Those were largely driven by earnings and were absorbed by the Blue Chip barometer during the month.

Of course this has led to some underperformance vis-a-vis the NASDAQ Composite (^IXIC) and S&P 500 (^SPX), but the ^DJI sitting just less than 1% from its closing high of 26,828 has to be considered a “win”.

The S&P 500 at 2945.83 posted a fresh closing high on the last day of April for gain of +3.9% on the month. The S&P is +17.5% YTD. The S&P has benefitted from solid gains the last 4 months by Technology, Energy, and even Health Care after a brief swoon in early April.

The NASDAQ Composite at 8095.39, added +4.7% in April to bring its outperformance in 2019 to +22% YTD. Social Media stocks have weathered the storm in large part from privacy and cyber security issues.

Semiconductors have had sharp gains until a couple of earnings faux pas — Intel Corp (INTC), this means you — just in the last week. Old-School-Tech has benefitted from Cap-Ex spending-fueled upgrades that have been overdue in the corporate world.

Note the string of fresh ATHs by Microsoft Corporation (MSFT) in the last month.

The NASDAQ posted a number of ATHs of late, most recently on April 29 with a print of 8161.85. Of course Tuesdays set back was largely attributable to the “Hot Mess” of an earnings report from Google.

The Russell 2000 (^RUT) at 1591.21 gained +3.3% in April and was +18% YTD. While the Russell is “in line” with the larger capitalization Major Market Averages, it has struggled to get through the 1600 level. The Russell is also at an 8.6% deficit to its closing high of 1740.75 from August 31 of last year.

We would really like to see the Russell 2000 get through its immediate resistance at the 1600 level. It has a history of rallying into its annual reconstitution late in late June, which this year is set for June 28. One positive sign is the Russell has held above the 200 day moving average for close to 2 weeks, the longest stretch since early October last year.

Put these Gains in Perspective

Although, stocks are off to a great start one-third of the way through 2019, we are faced with one caveat and one big question. The caveat is that not only is it unrealistic to expect current YTD returns will be annualized, we also need the perspective that measuring gains from year end 2018 lacks proper context. While it has long been convention to gauge performance by the calendar, It’s extremely rare to have extreme market volatility in late December. The S&P 500 lost over -11% in 7 trading days from December 13 to the 24th.

We think it would be most instructive to gauge where we are now off where the market closed on October 3 of last year. October 3 was the day that Federal Reserve Chairman Powell made his oft-referenced statement that base interest rates “were a long way from neutral”.

There is no dispute that FED watchers and market strategists viewed this as a definitive policy proclamation from the FED Chairman that alternate meeting rate hikes would continue well into 2019. The interpretation from most observers and strategists was that not until the base rate hit 3.5% at midyear 2019, would the FED reassess their position.

Throughout the market selloff during Q4, whenever the question of “What triggered this market downturn?” was posed, the near universal response was The Powell speech and Q&A in early October.

For Those Still With Me, Let’s Take a Look

Ironically, the Dow Jones Industrials made their ATH of 26.828.39 on October 3 of last year. At 26,593, the Dow was just shy of 1% from that ATH. With the damage done to individual stocks in the Dow of late, this is impressive.

The S&P 500 at 2945.83 is slightly less than +1% higher than where it closed on October 3 at 2925.51. Again, the S&P 500 currently sits at an ATH.

The NASDAQ Composite at 8095.39, like the S&P 500 is just less that +1% higher than were it settled on October 3 at 8025.09

The Russell 2000 at 1591.21 is -4.8% lower than it was on October 3 when it closed at 1671.29

So what’s the take away here? On the surface the Dow, S&P, and Nasdaq are all within 1% of our preferred October 3 gauge. We don’t like to see the Russell underperform to this extent, but the Big Three are pretty much where they were 7 months ago. Does that mean the rally has run its course? Should we anticipate a significant correction? Or worse?

Why the Market Landscape is Different

There is actually a very good case to be made that the market is much more attractive than it was last fall. There are a few critical macro valuation factors that support the case. I’ll make this very brief.

The FED has shifted its stance from hiking rates to neutral. Yes, they are still “tightening” a bit letting bonds in their balance sheet “run off”, but they have given a time table to wind that down by September of this year.

Economic Expansion marches on. Q1 GDP hit +3.2% last week, a full point higher than both Q1 and Q4 in 2018.

The interest rate on the benchmark 10 year treasury note is in a range of 2.50% to 2.60% compared to a range of 3.10% to 3.20% in early October last year.

Crude oil prices are approximately $8/barrel lower than last fall on both Brent Crude and West Texas Intermediate.

Inflation is lower. Core PCE; the FEDs preferred inflation gauge Is +1.7% year over year, compared to +2.0% last fall.

Obviously there are always fluid dynamics in the financial markets. In English, things can change in a hurry. However, in the static moment of early May 2019, we are in a more favorable environment than October 4 2018.

Industry production 4.0 and technology concept, depicting factory production on a conveyor belt with factory operational workers in uniform. (Photo: AdobeStock)

Factory orders, or new orders for manufactured goods, rose $9.3 billion or 1.9% to $508.2 billion in March, stronger than the consensus forecast.

The consensus forecast was looking for a 1.5% gain, ranging from a low of -0.5% to a high of 2.2%.

Prior

Revised

Consensus Forecast

Forecast Range

Actual

Factory Orders – M/M ∆

-0.5%

-0.3%

1.5%

-0.5% — 2.2%

1.9%

New Orders Durable Goods M/M ∆

-1.3%

—

—

—

2.6%

Shipments M/M ∆

0.2%

—

—

—

0.4%

Unfilled Orders M/M ∆

-0.2%

—

0.2%

Inventories M/M ∆

0.4%

—

0.3%

New orders for manufactured durable goods have been up four of the last five months, and increased $6.6 billion or 2.6% to $258.0 billion in March. That’s down slightly from the previously reported 2.7% gain, but up from the 1.3% decrease in February.

The upward revisions are a net positive for gross domestic product (GDP). The Bureau of Economic Analysis (BEA) “advance” estimate for Real GDP in Q1 2019 came in at an annual rate of 3.2%.

Transportation equipment also has been up four of the last five months, and led the increase in March by rising $6.1 billion or 7.0% to $93.8 billion.

New orders for manufactured nondurable goods rose $2.8 billion or 1.1% to $250.2 billion.

Shipments of manufactured durable goods have been up four of the last five months, and increased $1.0 billion or 0.4% to $259.5 billion in March. That’s up from the initially reported gain of 0.3% and follows a 0.2% increase in February.

Transportation equipment was up in March after two straight monthly declines, and drove the increase in shipments by rising $1.0 billion or 1.1% to $90.7 billion.

Shipments of manufactured nondurable goods have been up two consecutive months and rose $2.8 billion or 1.1% to $250.2 billion after gaining 0.8% in February.

Petroleum and coal products were also up two consecutive months, and drove the increase in nondurable shipments rising $3.2 billion or 6.0% to $55.5 billion.

Unfilled orders for manufactured durable goods in March have been up two of the last three months, and gained $2.7 billion or 0.2% to $1,181.2 billion in March.

While that’s down from the initially published 0.3% increase it follows a 0.2% decline in February. Transportation equipment drove the increase and is also up two of the last three months, rising $3.1 billion or 0.4% to $811.9 billion.

Inventories of manufactured durable goods have been up twenty‐six of the last twenty‐seven months, and gained $1.2 billion or 0.3% to $420.5 billion in March. That’s unchanged from the initially published increase and follows a decline of 0.4% in February.

Machinery has been up fifteen of the last sixteen months and led the increase in inventories for March, rising $0.7 billion or 1.0% to $71.7 billion.

Inventories of manufactured nondurable goods have been up three consecutive months, and rose $1.6 billion or 0.6% to $270.4 billion in March after gaining 0.2% in February. Petroleum and coal products have also been up three consecutive months and rose $1.2 billion or 3.0% to $41.5 billion in March

Materials and supplies decreased 0.1% in both durable goods and nondurable goods during March, regarding stage of production. Work in process rose 0.5% in durable goods and 1.1% in nondurable goods. Finished goods gained 0.5% in durable goods and 0.9% in nondurable goods.

What do you do when you face an unreasonable and irrational person in an argument? Tom discusses it on Liberty Never Sleeps.

The money pledged thru Patreon.com will go toward show costs such as advertising, server time, and broadcasting equipment. If we can get enough listeners, we will expand the show to two hours and hire additional staff.

To help our show out, please support us on Patreon.

All bumper music and sound clips are not owned by the show, are commentary, and of educational purposes, or de minimus effect, and not for monetary gain.

No copyright is claimed in any use of such materials and to the extent that material may appear to be infringed, I assert that such alleged infringement is permissible under fair use principles in U.S. copyright laws. If you believe material has been used in an unauthorized manner, please contact the poster.

A collage graphic concept for industry and labor. (Photo: AdobeStock)

Nonfarm business sector labor productivity rose sharply by 3.6% in the first quarter (Q1) 2019, beating the consensus and high end of the forecast range. The U.S. Bureau of Labor Statistics (BLS) said output gained 4.1% and hours worked rose by 0.5%.

Prior

Revised

Consensus Forecast

Forecast Range

Actual

Nonfarm Productivity – Q/Q ∆ – SAAR

1.9%

1.3%

1.9%

0.5% — 3.0%

3.6%

Unit Labor Costs – Q/Q ∆ – SAAR

2.0%

2.5%

1.8%

-0.5% — 3.0%

-0.9%

SAAR = Seasonally adjusted annual rate.

From Q1 2018 to Q1 2019, productivity rose 2.4%, representing a 3.9% gain in output and a 1.5% gain in hours worked. The four-quarter increase in labor productivity is the largest gain since Q3 2010, when it posted at 2.7%.

Unit labor costs in the nonfarm business sector declined 0.9% in Q1 2019, and gained 0.1% over the last four quarters. That’s the lowest four-quarter rate since Q4 2014, when it posted a 1.7% decrease.

Manufacturing sector labor productivity rose 1.7% in Q1 2019.

Labor productivity, or output per hour, is calculated by dividing an index of real output by an index of hours worked by all persons, including employees, proprietors, and unpaid family workers.

You have %%pigeonMeterAvailable%% free %%pigeonCopyPage%% remaining this month. Get unlimited access and support reader-funded, independent data journalism.