U.S. jobless claims graph on a tablet screen. (Photo: AdobeStock)

The Labor Department (DOL) said initial jobless claims came in at 211,000 for the week ending March 23, a decline of 5,000 and stronger than the forecast. The 4-week moving average fell to 217,250, a decline of 3,250 from the previous week’s revised average.

The consensus forecast for Q4 GDP was 225,000, ranging from a low of 220,000 to a high of 230,000.

The advance seasonally adjusted insured unemployment rate was unchanged at a historic low of 1.2% for the week ending March 16

No state was triggered “on” the Extended Benefits program during the week ending March 9.

The highest insured unemployment rates in the week ending March 9 were in Alaska (2.9), New Jersey (2.7), Montana (2.6), Connecticut (2.5), Rhode Island (2.5), Massachusetts (2.3), Pennsylvania (2.3), California (2.2), Illinois (2.1), and Minnesota (2.1).

The largest increases in initial claims for the week ending March 16 were in Oklahoma (+1,046), South Carolina (+270), California (+232), Tennessee (+221), and Mississippi (+211), while the largest decreases were in Illinois (-3,586), Oregon (-3,026), Pennsylvania (-2,242), Washington (-1,284), and Texas (-1,180).

Gross domestic product (GDP) graphic concept with yellow square pixels on a black matrix background. (Photo: AdobeStock)

The “third” estimate for fourth quarter (Q4) gross domestic product (GDP) came in at 2.2%, putting the annual growth rate at a solid 2.9%. While that’s down from 2.6% and 3.1%, respectively, it met the consensus forecast.

From Q4 2017 to Q4 2018, real GDP gained 3.0%, up from 2.5% in 2017.

The consensus forecast for Q4 GDP was 2.2%, ranging from a low of 1.8% to a high of 2.7%. The consensus for the price index was a unanimous 1.8%, while the 2.6% consensus for consumer spending ranged from 2.5% to 2.6%.

The price index for gross domestic purchases rose 1.7% in Q4 compared to 1.8% in Q3, just 0.1% off the forecast. The PCE price index gained 1.5%, compared to 1.6% in Q3.

Excluding food and energy prices, the PCE price index rose 1.8%, slightly more than the increase of 1.6% in Q3.

Real gross domestic income (GDI) increased 1.7% in Q4, compared with an increase of 4.6% in Q3. The average of real GDP and real GDI, which is a supplemental measure of U.S. economic activity that equally weights GDP and GDI, rose 1.9% in Q4 juxtaposed to an increase of 4.0% in Q3.

GDP 2018

As stated, real GDP rose 2.9% for 2018, while current-dollar GDP increased 5.2%, or $1.01 trillion, to a level of $20.49 trillion. The latter compares with an increase of 4.2%, or $778.2 billion, in 2017.

Real GDI increased 2.4% in 2018, compared with an increase of 2.3% in 2017.

On this episode of Liberty Never Sleeps, Tom argues government should be limited, decentralized and based on free market trade, not government oversight.

The money pledged thru Patreon.com will go toward show costs such as advertising, server time, and broadcasting equipment. If we can get enough listeners, we will expand the show to two hours and hire additional staff.

All bumper music and sound clips are not owned by the show, are commentary, and of educational purposes, or de minimus effect, and not for monetary gain.

No copyright is claimed in any use of such materials and to the extent that material may appear to be infringed, I assert that such alleged infringement is permissible under fair use principles in U.S. copyright laws. If you believe material has been used in an unauthorized manner, please contact the poster.

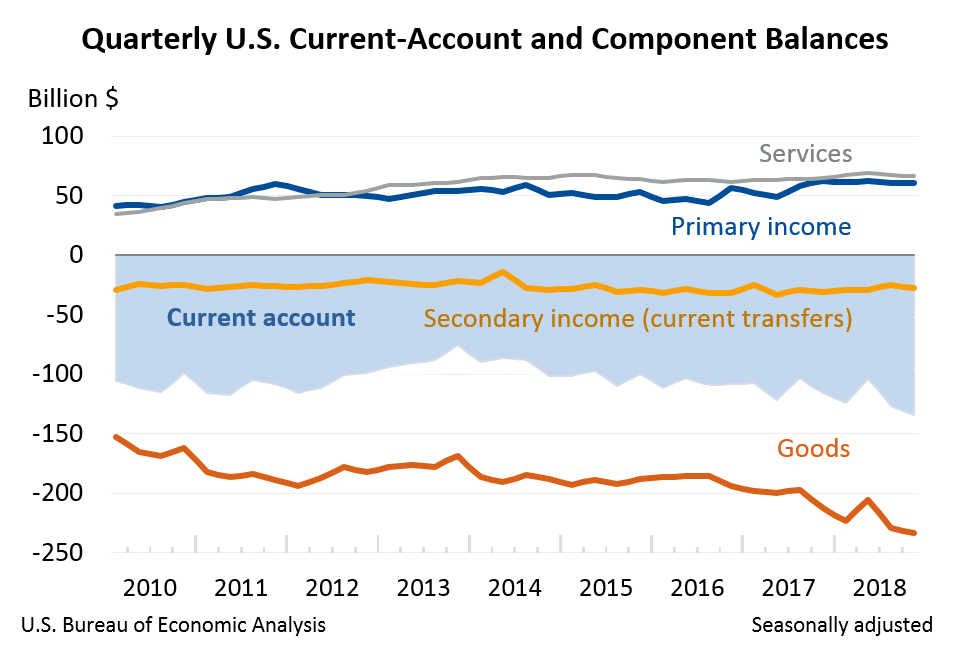

Current account balance concept: painted green text Current Account on digital data paper background with currency. (Photo: AdobeStock)

The U.S. current-account deficit preliminary read rose to $134.4 billion in the fourth quarter (Q4) 2018, up from a revised $126.6 billion for Q3.

According to statistics released by the Bureau of Economic Analysis (BEA), the deficit was 2.6% of current-dollar gross domestic product (GDP) in the fourth quarter, up from 2.5% in the third quarter.

The $7.8 billion increase in the current-account deficit was primarily driven by an increase in the deficits on goods, on secondary income and a decrease in the surplus on services.

Worth noting, the U.S. trade deficit also reported by the BEA on Wednesday narrowed far more than expected in January, indicating a potential reversal from Q4.

Exports of goods and services and income receipts increased $4.1 billion in the fourth quarter to $934.3 billion, while imports of goods and services and income payments increased $11.8 billion in Q4 to $1.1 trillion.

The money pledged thru Patreon.com will go toward show costs such as advertising, server time, and broadcasting equipment. If we can get enough listeners, we will expand the show to two hours and hire additional staff.

All bumper music and sound clips are not owned by the show, are commentary, and of educational purposes, or de minimus effect, and not for monetary gain.

No copyright is claimed in any use of such materials and to the extent that material may appear to be infringed, I assert that such alleged infringement is permissible under fair use principles in U.S. copyright laws. If you believe material has been used in an unauthorized manner, please contact the poster.

Year-Over-Year, Trade Deficit for Goods and Services Declined $1.9 billion, or 3.7 Percent

Import, Export, Logistics concept – Map global partner connection of Container Cargo freight ship for Logistic Import Export background (Photo: AdobeStock/Elements of this image furnished by NASA)

The U.S. trade deficit narrowed far more than expected in January, closing $8.8 billion to $51.1 billion and beating the consensus forecast.

The consensus forecast for the report released by U.S. Census Bureau and the U.S. Bureau of Economic Analysis (BEA) was $-57.3 billion, ranging from $59.0 billion to $55.0 billion.

In January, exports came in at $207.3 billion, $1.9 billion more than in December. Imports were $258.5 billion, $6.8 billion less than December.

The overall narrowing in the trade deficit for goods and services was fueled by a $8.2 billion decline in the goods deficit to $73.3 billion and an increase in the services surplus of $0.5 billion to $22.1 billion.

Year-over-year, the goods and services deficit decreased $1.9 billion, or 3.7%, from January 2018. Exports increased $6.1 billion or 3.0%. Imports increased $4.1 billion or 1.6%.

The average trade deficit for goods and services fell $1.8 billion to $53.9 billion for the three months ending January. Average exports declined $1.1 billion to $207.4 billion, while average imports fell $2.9 billion to $261.2 billion.

Year-over-year, the three-month average goods and services deficit gained $2.5 billion.

Goods By Selected Countries and Areas

The deficit with China decreased $5.5 billion to $33.2 billion in January. Exports decreased $0.2 billion to $7.5 billion and imports decreased $5.7 billion to $40.8 billion.

Goods and Services by Selected Countries and Areas

For the fourth quarter (Q4), the U.S. held trade surpluses in the billions of dollars with South and Central America ($21.2), Hong Kong ($8.1), Brazil ($7.4), United Kingdom ($4.9), Singapore ($4.8), Canada ($1.5), and OPEC ($0.6).

Deficits were posted in the billions of dollars with China ($102.6), the European Union ($28.7), Mexico ($21.4), Germany ($16.3), Japan ($14.1), Italy ($9.4), India ($5.8), Taiwan ($3.9), France ($3.0), Saudi Arabia ($2.7), and South Korea ($1.8).

The politically-sensitive trade deficit with China widened $6.3 billion to $102.6 billion in Q4. Exports fell $8.2 billion to $37.2 billion, as did imports by $1.9 billion to $139.8 billion.

The balance with Canada shifted from a deficit of $3.4 billion to a surplus of $1.5 billion in Q4. Exports decreased $0.8 billion to $89.1 billion and imports decreased $5.8 billion to $87.6 billion.

Howard Schultz, the former head of Starbucks Corporation, an American coffee company and coffeehouse chain founded in Seattle, Washington in 1971.

The possibility of former Starbucks CEO Howard Schultz mounting an independent run for the presidency in 2020 has unleashed a torrent of venomous personal attacks. For a third party candidate, the intensity of the attack has not been seen since Ross Perot in 1982.

Why Schultz, hardly a household name, has been the subject of such vituperation from the left, is made clear when the presidential polling is examined.

In every poll to date that included Schultz, support for the Democratic candidate was reduced, while the president is either unharmed or in a stronger position.

In the majority of cases, he is better off, with the Democratic candidate losing 1 to 9 points. Having obtained the services of Steve Schmidt, the former campaign manager for John McCain, it would Mr. Schultz has made his decision.

Mr. Schultz has apparently chosen to ignore Schmidt’s “going rogue” after McCain’s loss, attacking Sarah Palin and assigning blame to anyone but himself. Governor Palin, the 2008 vice presidential nominee, energized the moribund campaign, while Mr. Schmidt became the “Republican” commentator for the ultra-leftwing MSNBC.

Perhaps Mr. Schultz has wisely insisted on a post-campaign confidentiality agreement in their contract.

Schultz has even gone so far as to admit being unsure if he would have a woman as his vice-presidential running mate. It may be that he is waiting to see if Joe Biden declares.

It would be harder for Schultz to mount an, “I am the only voice of stability and reason” messaged campaign if Mr. Biden was to become the nominee. That case would be stronger if Bernie Sanders or Francis “Beto” O’Rourke were to win the nomination.

In head-to-head polling, Mr. Biden suffers the least from a Schultz candidacy as opposed to Kamala Harris and Elizabeth Warren, both of whom are hard hit.

The “progressive” nominees suffer the most from Schultz, which is clearly the reason he has been under a constant stream of vicious attacks by the likes of Wonkette and other progressive outlets.

Whomever becomes the Democratic nominee should be of no concern to Mr. Schultz. A new USA Today Suffolk Poll shows enormous potential for his third-party bid, far beyond the 12% he himself polled in the 3-way.

President Trump held a slight 3-point lead over a generic Democratic candidate candidate, 39% to 36%. But 11% chose a third-party and another 14% were undecided.

If he is hesitating, the survey should encourage him to prepare for his run.

Eleven percent (11%) of potential voters said they would vote for a third party candidate. With Mr. Schultz being the only serious third-party candidate, it is reasonable to expect he would garner the lion’s share. The residual Libertarian/Green vote is likely to be squashed even further than the desultory 4% they received combined in 2016.

As was seen in the head-to-head polling, Mr. Schultz received as high as 12% and, with a potential pool of a further 14% undecided to tap into, he could very well be a serious candidate with the ability to outperform Ross Perot. In 1992, Mr. Perot received 19% and 19.7 million votes as he would presumably be seen as a more serious and stable alternative.

On current polling, a Schultz run is most certainly viable, would be seriously detrimental to the Democratic Party and could ensure President Trump’s re-election in an Electoral College landslide.

Statistic graphic concept of the New York Stock Exchange (NYSE) Building in the Lower Manhattan Financial District, New York City. (Photo: Tomasz Zajda/AdobeStock/PPD)

Stocks closed with solid gains Tuesday, although well off their best levels of the day as investors are undeterred by soft reports on February housing activity and a weaker than expected consumer confidence report for March.

Bond yields rose for the first time in a week, tapping down some of the “fear factor” that had yields plunging late last week when the yield curve went “inverted” from 90 days to 10 years and the benchmark 10-Year Treasury Yield (US10YBY) note hit its lowest yield since late 2017.

There is no doubt stocks ran into stiff resistance as they approached last weeks highs, as early gains of better than +1% faded from late morning until mid afternoon.

Similar to yesterday, buyers became more aggressive during the last 90 minutes of trading as investors used the midday weakness to deploy idle cash reserves.

We’ve always placed a premium on the Last Hour Indicator when it shows a trend, and we’ll be watching closely for this as we begin a new month and quarter next week.

Market internals provided additional encouragement for investors, as advancing issues outpaced decliners by nearly 3 to 1 and Up Volume ran at 4x Down Volume.

If Major Market Averages can hold close to these levels, they’re poised to log the best quarterly performance since Q3 of 2009. This was of course the rally coming off the March 2009 lows following the 2008/09 Global Financial Crisis.

The Dow Jones Industrial Average (^DJI) gained +140.90 or +0.6% to 25,767. The DJIA is -1.0% this month and +10.0% YTD. The DJI is clearly lagging other market indices this month, primarily due to the weakness in Boeing Co (BA).

BA is lower by -$70 or -15.9% this month to $370. The decline this month in BA is responsible for nearly a 500 point decline in the DJI this month.

The S&P 500 rallied +20.10 or +0.7% to 2818.46. The S&P 500 (^SPX) is +1.2% in March, and +12.5% YTD. Technology and Energy stocks have been the two big drivers for S&P performance this quarter while Financials have clearly lagged.

The NASDAQ Composite (^IXIC) gained +56.00 or +0.7% to 7691.52. The NASDAQ has added +2.1% in March, and has outperformed other market averages this year with a gain so far of +16% YTD.

The NASDAQ is -2% off its recent high from last Thursday. We wouldn’t be surprised to see additional profit taking in names with outsized gains the last 3 days of this quarter. That could converge the YTD/QTD performance metrics between the NASDAQ and S&P 500 and DJI before quarters end on Friday.

Current Conditions Fueled Decline in Consumer Confidence

People count money at Macy’s Herald Square store during the early opening of the Black Friday sales in the Manhattan borough of New York, November 26, 2015. (Photo: Reuters)

The Consumer Confidence Index declined to 124.1 in March, missing the forecast though still elevated. The consensus forecast was 133.0, ranging from a low of 130.0 to a high of 134.4.

“Consumer Confidence decreased in March after rebounding in February, with the Present Situation the main driver of this month’s decline,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board.

“Confidence has been somewhat volatile over the past few months, as consumers have had to weather volatility in the financial markets, a partial government shutdown and a very weak February jobs report.”

While unemployment declined to 3.8% and wages grew by 3% or greater for the seventh straight month, the headline jobs number missed by 160,000.

Unsurprisingly, consumers’ assessment of current conditions declined in March.

The percentage of consumers stating business conditions are “good” fell from 40.6% to 33.4%, while those saying business conditions are “bad” ticked up from 11.1% to 13.6%.

Consumers’ assessment of the labor market was less optimistic.

Those stating jobs are “plentiful” fell from 45.7% to 42.0%, while those claiming jobs are “hard to get” increased marginally from 11.7% to 13.7%.

“Despite these dynamics, consumers remain confident that the economy will continue expanding in the near term,” Franco added. “However, the overall trend in confidence has been softening since last summer, pointing to a moderation in economic growth.”

Consumers’ optimism about the short-term future moderated. The percentage of consumers expecting business conditions will improve over the next six months fell from 19.6% to 17.7%, while those expecting business conditions will worsen remained relatively flat, 9.3% versus 9.2% last month.

Consumers’ outlook for the labor market was less favorable.

The proportion expecting more jobs in the months ahead decreased from 19.0% to 16.4%, while those anticipating fewer jobs increased from 12.3% to 13.4%.

On short-term income prospects, the percentage of consumers expecting an improvement rose slightly, from 20.6% to 21.0%, while the proportion expecting a decline in income fell from 8.3% to 7.6%.

The Consumer Confidence Survey is based on a probability-design random sample, is conducted monthly for The Conference Board by Nielsen.

The cutoff date for the preliminary results was March 14.

An American flag flying behind barbed wire at the U.S. southern border with Mexico. (Photo: AdobeStock)

The Department of Defense (DOD) announced the transfer of $1 billion to construct 57 miles of 18-foot high border fencing, as well as other projects for the U.S Army Corps of Engineers.

“10 U.S.C. § 284(b)(7) gives the Department of Defense the authority to construct roads and fences and to install lighting to block drug-smuggling corridors across international boundaries of the United States in support of counter-narcotic activities of Federal law enforcement agencies,” the Pentagon said in a statement.

The Department of Homeland Security (DHS) and Customs and Border Protection requested the funds for the construction of a border wall.

This story is developing and will be updated as both sides of the debate return requests for comment.

You have %%pigeonMeterAvailable%% free %%pigeonCopyPage%% remaining this month. Get unlimited access and support reader-funded, independent data journalism.