On this episode of Liberty Never Sleeps, Tom argues the way to fight the liberal advance is by accepting loss and by forming a strategy to move forward with reason.

*On Blind Partisanship *The Players Are Lining Up *Medicare Please, with No ICE *Oh, BTW, Afghanistan *Where is RBG?

The money pledged thru Patreon.com will go toward show costs such as advertising, server time, and broadcasting equipment. If we can get enough listeners, we will expand the show to two hours and hire additional staff.

All bumper music and sound clips are not owned by the show, are commentary, and of educational purposes, or de minimus effect, and not for monetary gain.

No copyright is claimed in any use of such materials and to the extent that material may appear to be infringed, I assert that such alleged infringement is permissible under fair use principles in U.S. copyright laws. If you believe material has been used in an unauthorized manner, please contact the poster.

California Senator Kamala Harris, D-Calif., speaks during a committee hearing.

It seems like every Democrat in the country plans to run against Trump in 2020 and presumably all of them will feel compelled to issue manifestos outlining their policy agendas.

Which gives me lots of material for my daily column.

Today, let’s review the two big ideas that have been unveiled by Kamala Harris, the Senator from California who just announced her bid for the White House.

We’ll start with her idea to create a federal subsidy for rent payments. I wrote about this new handout last year, and warned that it would enrich landlords (much as tuition subsidies enrich colleges and health subsidies enrich providers).

Here’s some of what Professor Tyler Cowen wrote for Bloomberg about the proposal.

One of the worst tendencies in American politics is to restrict supply and subsidize demand. …The likely result of such policies is high and rising prices, restricted access and often poor quality. If you limit the number of homes and apartments, for example, but give buyers subsidies, that is a formula for exorbitant prices. That is what makes early accounts of Senator Kamala Harris’s economic plans so disappointing. …Consider Harris’s embrace of subsidies for renters, as reflected by her recent sponsorship of the Rent Relief Act of 2018. Given the high price of housing in many parts of the U.S., it is easy to see why the idea might have appeal. But the best and most sustainable way of producing cheaper housing is to build more homes and apartments. The resulting increase in supply will cause prices to fall… That is basic supply and demand, with supply doing the active work. The Harris bill, in contrast, calls for tax credits to renters. …There is an obvious problem with this approach. If you subsidize renters, that will push up the price of apartments. Furthermore, economic logic suggests that big rent increases are most likely in those cases where the supply of apartments is relatively fixed, a basic principle of what is called “tax incidence theory.” In sum, most of the gains from this policy would go to landlords, not renters.

In other words, this is a perfect plan for a politician who understands “public choice” theory.

Ordinary voters think they’re getting a freebie, but the benefits actually go to those with political influence and power.

Now let’s look at her $2.7 trillion tax cut. I believe that people should be allowed to keep the lion’s share of any money they earn, so my gut instinct is to cheer.

But it’s always good to be skeptical when a politician is offering something that sounds too good to be true.

Kyle Pomerlau of the Tax Foundation has done the heavy lifting and looked closely at the details. He has a thorough explanation of her plan and its likely impact.

The “LIFT the Middle-Class Act” (LIFT) would create a new refundable tax credit available to low- and middle-income taxpayers. …LIFT would provide a refundable credit that would match a maximum of $3,000 in earned income ($6,000 for married couples filing jointly). …The credit would begin to phase out for single taxpayers starting at $30,000 of adjusted gross income (AGI) and $80,000 for single taxpayers with children, and begin phasing out for married taxpayers at $60,000 of AGI. The phaseout rate for all taxpayers would be 15 percent. …LIFT’s impact on the economy is primarily through its effect on the labor force. LIFT phases in from the first dollar of earned income to the maximum credit of $3,000 per tax filer. It then phases out starting at different levels of income, depending on a tax filer’s marital status and whether they have children. These phase-ins and phaseouts create implicit marginal subsidies and tax rates that impact individuals’ incentive to work.

And that means some taxpayers get subsidized for working and some taxpayers get penalized.

For taxpayers in the credit phaseout range, tax liability would increase by 15 cents for each additional dollar earned. This means that these taxpayers would face an additional implicit marginal tax rate of 15 percent, which would reduce these taxpayers’ incentive to work additional hours. In contrast, taxpayers in the phase-in range of the credit would get $1 for each additional $1 of income they earn. As such, these taxpayers would benefit from an effective marginal subsidy rate, or negative marginal tax rate, of 100 percent. A negative tax rate of 100 percent would increase the incentive for these taxpayers to work additional hours.

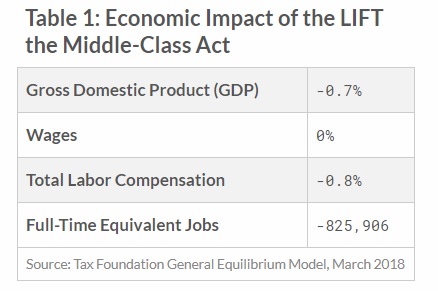

Kyle crunches the numbers to determine the overall economic impact.

While the positive labor force effects of the phase-in of the credit could offset the negative effect of the phaseout, we find that, on net, the size of the total labor force would shrink under this policy. This is primarily due to the large number of taxpayers that would fall in the phaseout range of the credit relative to the number of individuals that would benefit from the phase-in. …We estimate that the credit…would reduce economic output by 0.7 percent and result in about 825,906 fewer full-time equivalent jobs.

Here’s the relevant table from the Tax Foundation’s report.

Source: Tax Foundation

This is remarkable. It would seem impossible to design a $2.7 trillion tax cut that actually hurts the economy, but Sen. Harris has succeeded in that dubious achievement.

For all intents and purposes, she has figured out how to have an anti-supply-side tax cut.

And there are two other problems that deserve attention.

First, as noted in Kyle’s paper, the tax cut is “refundable.” This means that money goes to people who don’t pay taxes. In other words, it is government spending being laundered through the tax code. So Harris claims to be cutting taxes, but part of what she’s doing is expanding redistribution and making government bigger, and encouraging more fraud.

Second, Harris is very cagey about how the numbers work in her proposal. Does she want the tax cuts (and new spending) financed by more borrowing? By printing money? By offsetting class-warfare tax increases? Some combination of the three? Whatever the answer, the negative economic damage will be substantially higher if financing costs are included.

Considering the poor design and upside-down economics of the rent subsidy scheme and the new tax credit, the bottom line is rather obvious: Kamala Harris wants to buy votes, and she has decided that it is okay to hurt the economy in hopes of achieving her political ambitions.

Consumer confidence 3D gear graphic reporting the Conference Board Consumer Confidence Index.

The Conference Board Consumer Confidence Index declined in January to 120.2 (1985=100), a still elevated reading that missed the consensus forecast.

Forecasts ranged from a low of 119.1 to a high of 129.0, with the consensus at 124.3. It follows a decline in December, but was somewhat expected and most likely temporary.

“Consumer Confidence declined in January, following a decrease in December,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board. “The Present Situation Index was virtually unchanged, suggesting economic conditions remain favorable.”

“Expectations, however, declined sharply as financial market volatility and the government shutdown appear to have impacted consumers.”

The Present Situation Index – which measures consumers’ assessment of current business and labor market conditions – declined only marginally, from 169.9 to 169.6.

The Expectations Index – which gauges consumers’ short-term outlook for income, business and labor market conditions – declined from 97.7 last month to 87.3 this month.

“Shock events such as government shutdowns (i.e. 2013) tend to have sharp, but temporary, impacts on consumer confidence,” Franco added. “Thus, it appears that this month’s decline is more the result of a temporary shock than a precursor to a significant slowdown in the coming months.”

Consumers’ views of current conditions remain positive and were little changed in January.

The percentage of consumers claiming business conditions are “good” was essentially unchanged at 37.4 percent, while those saying business conditions are “bad” actually decreased from 11.6 percent to 11.1 percent.

Consumers’ assessment of the labor market was mixed.

Those stating jobs are “plentiful” rose from 45.5 percent to 46.6 percent, while those claiming jobs are “hard to get” also rose, from 12.2 percent to 12.9 percent.

Not surprising, given events and coverage of those events, consumers were less optimistic about the short-term future in January.

The percentage of consumers expecting business conditions will improve over the next six months ticked down from 18.1 percent to 16.0 percent, while those expecting business conditions will worsen moved higher from 10.6 percent to 14.8 percent.

Consumers’ outlook for the labor market was also less optimistic.

The proportion expecting more jobs in the months ahead decreased from 16.6 percent to 14.7 percent, while those anticipating fewer jobs increased, from 14.6 percent to 16.5 percent.

Meanwhile, the percentage of consumers expecting an improvement to short-term income prospects fell from 22.4 percent to 18.2 percent. However, the proportion expecting a decrease also fell, from 7.6 percent to 7.1 percent.

About the Consumer Confidence Index

The monthly Consumer Confidence Survey is based on a probability-design random sample, is conducted for The Conference Board by Nielsen, a leading global provider of information and analytics around what consumers buy and watch. The cutoff date for the preliminary results was January 17.

Declining Existing Home Sales, Affordability the Major Factors in Slowing Home Price Gains

Real Estate Market Going Up Concept Illustration. (Photo: AdobeStock)

The S&P CoreLogic Case-Shiller Home Price Index (HPI) covering all nine U.S. census divisions posted a 5.2% annual gain in November. That’s down from 5.3% in the previous month.

The 10-City Composite came in at an annual gain of 4.3%, down from 4.7% in the previous month. The 20-City Composite posted a 4.7% year-over-year gain, down from 5.0% in the previous month and slightly missing the 4.9% consensus forecast.

“Home prices are still rising, but more slowly than in recent months,” says David M. Blitzer, Managing Director and Chairman of the Index Committee at S&P Dow Jones Indices. “The pace of price increases are being dampened by declining sales of existing homes and weaker affordability.”

Buyers pulled back before Fed policy changed course in December, and mortgage rates eased, down to 4.45% from 4.95%.

“Sales peaked in November 2017 and drifted down through 2018,” Mr. Blitzer added. “Affordability reflects higher prices and increased mortgage rates through much of last year.”

Las Vegas, Phoenix and Seattle reported the highest year-over-year gains among the 20 cities. Las Vegas led the way with a 12.0% year-over-year price increase, followed by Phoenix at 8.1% and Seattle at 6.3%.

“Housing market conditions are mixed while analysts’ comments express concerns that housing is weakening and could affect the broader economy,” Mr. Blitzer continued. “Current low inventories of homes for sale – about a four-month supply – are supporting home prices.”

Before seasonal adjustment, the National Index posted a month-over-month gain of 0.1% in November. The 10-City and 20-City Composites both reported a 0.1% decrease for the month. After seasonal adjustment, the National Index recorded a 0.4% month-over-month increase in November.

The 10-City Composite and the 20-City Composite both posted 0.3% month-over-month increases. In November, eight of 20 cities reported increases before seasonal adjustment, while 15 of 20 cities reported increases after seasonal adjustment.

“New home construction trends, like sales of existing homes, peaked in late 2017 and are flat to down since then,” Mr. Blitzer noted. “Stable 2% inflation, continued employment growth, and rising wages are all favorable.”

“Measures of consumer debt and debt service do not suggest any immediate problems.”

Federal grand juries have returned indictments against Huawei, its CFO Wanzhou Meng, several affiliates, and one of its subsidiaries here in the United States.

Acting Attorney General Matthew G. Whitaker announced a grand jury in Seattle has returned an indictment alleging 10 federal crimes by two affiliates of Chinese telecommunications conglomerate Huawei Technologies.

Further, he also announced a grand jury in the Eastern District of New York returned a 13-count indictment alleging additional crimes committed by Huawei, its CFO, its affiliate in Iran, and one of its subsidiaries Huawei Device Co. USA.

The criminal activity alleged in this indictment, which has been assigned to U.S. District Judge Ann M. Donnelly, goes back at least 10 years and goes all the way to the top of the company.

“Today we are announcing that we are bringing criminal charges against telecommunications giant Huawei and its associates for nearly two dozen alleged crimes” Acting Attorney General Matthew G. Whitaker said. “As I told Chinese officials in August, China must hold its citizens and Chinese companies accountable for complying with the law.”

Huawei is the world’s biggest supplier of network gear used by cellular phone and Internet companies. The charges include bank fraud, conspiracy to commit wire fraud and violating the International Emergency Economic Powers Act.

According to the indictment, in 2012 Huawei began a concerted effort to steal information about a robot that T-Mobile used to test mobile phones, all part of an effort to build their own.

Huawei’s engineers allegedly violated confidentiality and non-disclosure agreements with T-Mobile by secretly taking photos of the robot, measuring it, and stealing a piece of it.

“For years, Chinese firms have broken our export laws and undermined sanctions, often using U.S. financial systems to facilitate their illegal activities,” Commerce Secretary Wilbur Ross said. “This will end. The Trump Administration continues to be tougher on those who violate our export control laws than any administration in history. “

The federal government alleges Huawei became aware of the government’s investigation in 2017, and along with its subsidiary Huawei USA tried to obstruct the investigation by moving witnesses with knowledge of Huawei’s Iran-based business to the People’s Republic of China.

The indictment further alleges Huawei tried to conceal and destroy evidence of Huawei’s Iran-based business located in the United States.

In December 2018, Canadian authorities arrested Meng in Vancouver on a provisional arrest warrant. The U.S. government is now seeking Meng’s extradition.

President Donald Trump signs an executive order, left, while Venezuela’s President Nicolas Maduro, right, attends a signing ceremony. (Photos: Reuters/Miraflores Palace/Handout)

The Trump Administration on Monday announced sanctions targeting Nicolás Maduro through Venezuela’s state-owned oil and natural gas monopoly.

Petróleos de Venezuela, S.A. (PdVSA), translated to Petroleum of Venezuela, was founded on January 1, 1976 with the nationalization of the Venezuelan oil industry. Since that founding, it has dominated the nation’s oil industry, and became the world’s fifth largest oil exporter.

“The United States is holding accountable those responsible for Venezuela’s tragic decline, and will continue to use the full suite of its diplomatic and economic tools to support Interim President Juan Guaidó, the National Assembly, and the Venezuelan people’s efforts to restore their democracy,” said Secretary of the Treasury Steven T. Mnuchin.

“Today’s designation of PdVSA will help prevent further diverting of Venezuela’s assets by Maduro and preserve these assets for the people of Venezuela,” Secretary Mnuchin added. “The path to sanctions relief for PdVSA is through the expeditious transfer of control to the Interim President or a subsequent, democratically elected government.”

Oil reserves in Venezuela are the largest in the world, totaling 297 billion barrels (4.72×1010 m3) as of January 1, 2014. The state-owned monopoly has converted those resources into significant funding to the regime.

Venezuela has 77.5 billion barrels (1.232×1010 m3) of conventional oil reserves according to PdVSA figures, the largest in the Western Hemisphere and making up approximately half the total.

Following the Bolivarian Revolution, PdVSA was mainly used as a political tool of the government. Between 2004 and 2010, PdVSA contributed $61.4 billion to the government’s social development projects, with around half of that going directly to various Bolivarian Missions.

The remainder was distributed via the National Development Fund. But profits are also used to assist the presidency, with funds directed towards allies of the Venezuelan government.

In this sense, these new sanctions target the personal wealth of and political support for Nicolás Maduro, the invalidated Venezuelan president struggling to hang on to power.

Last week, President Donald Trump recognized Juan Guaidó as the Interim President of Venezuela. Since the U.S. made the decision, 21 additional nations have taken the same steps.

“I call on all responsible nations to immediately recognize interim President Guaidó,” National Security Advisor John Bolton said. “Now is the time to stand with democracy and prosperity in Venezuela.”

But I also feel sorry for taxpayers, who are bearing ever-higher costs to finance redistribution programs.

Today’s column won’t focus on those issues. Instead, we’re going to utilize new OECD data to compare the size of the welfare states in developed nations.

We’ll start with the big picture. Here it total redistribution spending, measured as a share of economic output, for selected countries that are members of the Organization for Economic Cooperation and Development.

Nobody will be surprised, I assume, to see that France, Finland, Belgium, Denmark, and Italy have the biggest welfare states.

The United States is in the middle of the pack. American taxpayers might be surprised to learn, though, that they finance a bigger welfare state than the ones that exist in Canada, Iceland, and the Netherlands.

The overall numbers are important, but it’s also educational to consider the various components.

And the largest chunk of social spending in most nations is for their old-age programs. The biggest burdens are found in Greece, Italy, France, Portugal, and Austria. The United States, once again, is in the middle of the pack.

By the way, keep in mind that there are many factors that determine why some nations spend more than others.

How generous are benefits? – This is often measured as the “replacement rate,” which compares retirement benefits to income during working years.

When can people retire? – Some countries allow people, or some classes of people, to get benefits while relatively young. Others are more stringent.

Does a country have an aging population? – Demographic changes already are beginning to have a large effect on the finances of some systems.

Is there a private savings system? – Nations such as Switzerland, Australia, Chile, and the Netherlands have significant private retirement savings.

Now let’s look at government spending on health.

Here’s the area where the United States is more extravagant than almost every other nation. Only France spends more money.

Actually, since per-capita GDP is significantly larger in the United States than in France, American taxpayers spend more on a per-person basis.

Some people will observe, with great justification, that the data for the United States may be a measure of the inefficiency of the American system rather than taxpayer generosity. This is a topic for another day.

Last but not least, let’s look at traditional welfare. In other words, cash assistance to the working-age population.

The fiscal burden of this spending is highest in Belgium, Finland, the Netherlands, Norway, and Luxembourg. The United States, meanwhile, is comparatively frugal.

P.S. Here are a couple of caveats for number crunchers and policy wonks.

First, there are methodological challenges when comparing OECD nations. Eastern European nations tend to be significantly less prosperous than Western European nations, thanks to decades of communist enslavement. So looking at this data does not really allow for apples-to-apples comparisons. Moreover, there are a handful of developing nations that belong to the OECD, such as Mexico and Turkey, so comparison are effectively meaningless. And Chile is on the cusp of becoming a fully developed nation so it’s in its own category.

Second, as I briefly mentioned above, nations have different levels of per-capita GDP. If we look at the last chart, Austria and Spain spend a similar share of GDP on welfare, but since Austria is a richer nation, its taxpayers actually finance a lot more per-capita welfare spending. The same is true if you compare Canada and Estonia, Sweden and Slovenia, and Germany and Greece.

Double exposure of security check airport sign. Airport security check at gates with metal detector and scanner. (Photo: AdobeStock)

My previous columns about the Transportation Security Administration (TSA) have focused on bureaucratic inefficiency and incompetence (as well as laughable examples of “security theater”).

Today, let’s take advantage of the shutdown and focus instead on why TSA should be disbanded so that airports can use more efficient private security firms.

An article in Reason gives some important details on why privatized airport screening is the best way of making lemonade out of shutdown lemons.

…the Transportation Security Administration (TSA) reported that 10 percent of its agents were absent from their posts, up from three percent in the same time period last year. …The result has been longer wait times, closed security checkpoints… While it’s difficult to feel any sympathy at all for the professional privacy violators at the TSA… It’s also an unfortunate consequence of federalizing so much of crucial airport operations, says Baruch Feigenbaum, a transportation expert… There are already a number of airports in the country that have contracted out their passenger screenings to private companies through the TSA’s Screening Partnership Program (SPP), helping to immunize them from the effects of the shutdown. This includes San Francisco International Airport (the busiest airport to participate in the SPP program), where some 1,200 privately employed security screeners have continued to be paid despite all the budget drama in Washington. …Contracting out these services would ensure that they don’t come to a screeching halt every time the government shuts down. Putting that distance between the government and security and safety services would also improve oversight.

For all intents and purposes, the folks at Reason want to make a virtue out of necessity. The government shutdown is making air travel an even bigger hassle, so why “let a crisis go to waste” when this is a great opportunity to push for sweeping reform?

As a frequent flyer, I say Amen.

Here’s a good example. Because of my support for the Georgia Bulldogs, I have to endure the Atlanta airport several times each year. It is one of the worst airports I’ve ever experienced.

It’s so bad that the city’s politicians are exploring private security.

Atlanta Mayor Kasim Reed…said he wants to take a closer look at privatizing security screening at the Atlanta airport to address the issue of long lines. …Southwell…earlier this year sent a letter to the Transportation Security Administration, raising the idea of privatizing security screening at the Atlanta airport if long lines were not addressed. …Reed said Monday that the city has been in conversations with San Francisco International Airport, which privatized its security screening. “We’re going to explore that and see if it’s the best decision,” Reed said. “The lines are very concerning to me…. We’re going to do every single thing we can do, and it’s going to have urgency to it.”

It’s quite possible that Atlanta’s politicians are merely bluffing and that their real goal is to simply get more TSA bureaucrats, but I hope this is a serious initiative and that Atlanta escapes the TSA.

For those who want to understand the background on this issue, here are a couple of very good articles.

The first piece, from Skift, explain how we got to the current situation.

Airports could actually do something about the hated agency, and a few are weighing a radical option: firing TSA screeners and hiring private replacements. The frustration over queue times—which have topped two and three hours at airports in Atlanta, Chicago, Charlotte and Denver—has prompted new attention by airport executives to the TSA’s little-known Screening Partnership Program, in which the federal agency solicits bids for a contractor to handle airport screening. The contractors must follow the same security protocols as federal officers, with similar wages and benefits. At Phoenix Sky Harbor International Airport, …administrators are “discussing a variety of options,” including replacing the TSA with a private contractor, said Deborah Ostreicher, assistant aviation director at the airport. Sky Harbor officials have considered their TSA service “less than satisfactory for many months,” she said. The Phoenix airport is a hub for American Airlines Group Inc., which has blamed the TSA delays across the country for causing more than 70,000 passengers to miss flights so far this year ….The former general manager of Atlanta’s Hartsfield-Jackson Airport wrote a letter to the TSA in February warning that the world’s busiest airport was “conducting exhaustive research” into privatized security screening.

There are 22 airports that already have opted out.

The power to replace TSA employees with private screeners dates to the birth of the agency in 2002, shortly after the Sept. 11th terrorist attacks. Congress designated five airports at the time to offer screening by private firms as a way to compare the federal approach. Another 17 smaller airports have since joined the original five. The most recent to make the switch to private security screeners, Punta Gorda Airport in Florida, expects to finish the transition next week. San Francisco International is the largest U.S. airport with private screeners. Now other large airports are researching private-sector alternatives.

One of the benefits of privatization is that contractors have more flexibility to do a better job.

…airports that have switched to private firms say they consider the contractors more responsive and better able to adjust staffing to address traffic surges and lulls. …said Brian Sprenger, director at Bozeman Yellowstone International Airport in Montana, which began private screening in 2014. “We now have a little bit more say in ensuring that the customer service side is a little more elevated in the process.”

Though TSA is reluctant to allow more airports to escape.

Christopher Bidwell, vice president of security for Airports Council International-North America, faulted the TSA in the past for making it difficult for airports to switch to private screeners, regularly denying airports’ applications for the program. …Any airport wishing to switch must be pass a security and cost analysis by the TSA to demonstrate that hiring private contractors will not harm the agency’s budget or compromise security.

A column in City Journal adds some more historical background, noting that the failures on 9/11 were the result of government guidelines.

Even by Washington standards, the creation of the TSA was a blunder of colossal proportions. Experts from around the world warned at the time—in 2001—that federalizing airport security would be ruinously expensive, inefficient, and unsafe. Israel and many European countries had already rejected similar systems. …Democrats who controlled the Senate were especially eager to gain campaign contributions from tens of thousands of new federal employees. …Legislators and bureaucrats scapegoated the private security companies that had been screening passengers for the airlines. Citing the lapse in security on September 11… It was the federal government, not the private screeners, that set the policy allowing small knives and box cutters to be brought onto planes. Federal guidelines prevented airlines from arming pilots and reinforcing cockpit doors. The feds also stopped the private security firms from using an existing system to identify high-risk passengers, which would have singled out some of the hijackers for special screening.

Here’s some great data on the superiority of private airport screeners.

…the TSA blames its failures on lack of funding. But it’s already spending way too much, as demonstrated in a congressional study comparing TSA screeners in Los Angeles with non-TSA screeners in San Francisco, one of the few airports allowed to run its own system, contracting with a private company. If LAX switched to the San Francisco model, the study concluded, it could cut its screening costs by more than 40 percent. The San Francisco private company’s screeners received the same salary and benefits as TSA screeners, but they were so much better trained and deployed that each one processed 65 percent more passengers than a TSA screener in Los Angeles. They apparently enjoyed better working conditions, too, because they were much less likely to quit their jobs. And in tests by federal investigators, they were three times better at detecting contraband.

Unfortunately, TSA has institutional hostility to private screeners.

Those results, as well as other research showing that private screeners get better ratings from passengers and airport managers, inspired congressional Republicans to pass legislation giving more airports the option of switching to private contractors. But, as anyone could have predicted in 2001, it’s not easy to get rid of a federal monopoly, especially now that unionized screeners can intimidate local politicians—as they did in blocking an attempt to replace them at Sacramento’s airport. Even if local officials stand up to the union, they still need to get permission from the TSA.

And, as noted in the Wall Street Journal, many politicians don’t care about the private sector’s superior performance because they’re more intreested in expanding bureaucracy.

TSA runs a Screening Partnership Program, which in theory allows an airport to “opt out” of TSA and bring in a certified private security firm. In a 2011 report, the House Committee on Transportation and Infrastructure compared Los Angeles data with a private operationrunning San Francisco’s airport. A contract screener in San Fran moved through 65% more passengers than TSA employees in L.A. But only a handful of airports participate, as TSA chooses the security company and micromanages the contract. That isn’t a partnership. Congress could stipulate that an airport manage its own bidding and operations; the government would remain a safety regulator. …Congress nationalized airport screening after 9/ll, as Democrats saw a political opening to add thousands of new union workers. But after nearly a decade and a half, TSA’s legend of incompetence grows.

Sadly, growing incompetence is not matched by growing pressure for privatization.

Industry production 4.0 and technology concept, depicting factory production on a conveyor belt with factory operational workers in uniform. (Photo: AdobeStock)

The Texas Manufacturing Outlook Survey indicated regional factory activity accelerated and continued to expand in January.

The production index, a key measure of state manufacturing conditions, nearly doubled from 7.3 to 14.5, indicating growth in output was heating up.

While most other measures of manufacturing activity also indicated continued growth in January, the pace of growth in demand slowed slightly.

The capacity utilization index increased seven points to 14.8, and the shipments index rose five points to 11.4. Meanwhile, the new orders index ticked down slightly to 11.6 and the growth rate of new orders index fell from 5.8 to 1.2.

However, views of broader business conditions improved in January.

The general business activity index rebounded from a multiyear low of -5.1 in December to 1.0 in January. This near-zero reading indicates regional manufacturers were fairly balanced in their views of whether activity had improved or worsened.

The company outlook index also rebounded from negative territory this month, gaining more than 10 points to 7.1.

The employment index retreated four points to 6.6, which is a two-year low. Sixteen percent of firms noted net hiring juxtaposed to 10 percent reporting net layoffs. The hours worked index ticked down to 3.6.

Upward pressure on input prices and wages eased again in January, while pressure on selling prices held steady.

The raw materials price index fell by eight points to 21.2, and the wages and benefits index ticked down two points to 27.4. Meanwhile, the finished goods price index was unchanged at 6.4.

Expectations regarding future business conditions were more positive in January. The indexes of future general business activity and future company outlook increased to 11.7 and 22.3, respectively.

An American Flag flying in front of a U.S. manufacturing factory. (Photo: AdobeStock)

The Chicago Fed National Activity Index (CFNAI) jumped +0.27 in December, up slightly from +0.21 in November and beating the +0.15 consensus forecast.

Without a doubt, the +1.1 jump in manufacturing within the production component was a major driver of the gain.

Two of the four broad categories of indicators that make up the index rose from November, while two of the four categories made positive contributions to the index in December.

The index’s three-month moving average, known as the CFNAI-MA3, also ticked up to +0.16 in December from +0.12 in November.

The CFNAI Diffusion Index, which is also a three-month moving average, rose +0.14 from +0.11 in November. Forty-six of the 85 individual indicators made positive contributions to the CFNAI in December, while 39 made negative contributions.

Forty indicators improved from November to December, while 44 indicators deteriorated and one was unchanged. Of the indicators that improved, ten made negative contributions.

Employment-related indicators contributed a steady +0.11 to the CFNAI in December, up slightly from +0.10 in November. Total nonfarm payrolls rose by 312,000 in December’s blockbuster jobs report, after increasing by a respectable 176,000 in the previous month.

About the CFNAI

H/T Chicago Federal Reserve:

The CFNAI is a weighted average of 85 existing monthly indicators of national economic activity. It is constructed to have an average value of zero and a standard deviation of one. Since economic activity tends toward trend growth rate over time, a positive index reading corresponds to growth above trend and a negative index reading corresponds to growth below trend.

The 85 economic indicators that are included in the CFNAI are drawn from four broad categories of data: production and income; employment, unemployment, and hours; personal consumption and housing; and sales, orders, and inventories. Each of these data series measures some aspect of overall macroeconomic activity. The derived index provides a single, summary measure of a factor common to these national economic data.

You have %%pigeonMeterAvailable%% free %%pigeonCopyPage%% remaining this month. Get unlimited access and support reader-funded, independent data journalism.