Tom wraps it all up these week. With the advent of modern science and the death of Bush, we really have come to a make or break point insofar as our need for big government in our lives.

Bumper Music:

Music provided by “Solo Guitar” by Yan Terrien in conjunction with Freemusic.org.

Closing Music

http://www.hulkshare.com/praktikos/dark-nights-rise

The money pledged thru Patreon.com will go toward show costs such as advertising, server time, and broadcasting equipment. If we can get enough listeners, we will expand the show to two hours and hire additional staff.

To help our show out, please support us on Patreon: https://www.patreon.com/LibertyNeverSleeps

All bumper music and sound clips are not owned by the show, are commentary, and of educational purposes, or de minimus effect, and not for monetary gain.

No copyright is claimed in any use of such materials and to the extent that material may appear to be infringed, I assert that such alleged infringement is permissible under fair use principles in U.S. copyright laws. If you believe material has been used in an unauthorized manner, please contact the poster.

The Paris riots are only superficially about the increased fuel tax, what they are really rioting over is the right of self determination and the elites in society.

Music provided by “Solo Guitar” by Matt LeGroulx in conjunction with Freemusic.org.

Closing Music

http://www.hulkshare.com/praktikos/dark-nights-rise

The money pledged thru Patreon.com will go toward show costs such as advertising, server time, and broadcasting equipment. If we can get enough listeners, we will expand the show to two hours and hire additional staff.

To help our show out, please support us on Patreon: https://www.patreon.com/LibertyNeverSleeps

All bumper music and sound clips are not owned by the show, are commentary, and of educational purposes, or de minimus effect, and not for monetary gain.

No copyright is claimed in any use of such materials and to the extent that material may appear to be infringed, I assert that such alleged infringement is permissible under fair use principles in U.S. copyright laws. If you believe material has been used in an unauthorized manner, please contact the poster.

Buying American Made Cars. Supporting the American auto industry and economy photomontage with automobiles and the American Flag. (Photo: AdobeStock)

Sales of U.S. light motor vehicles came in at 17.49 million units (SAAR) in November, near the 12-month high and beating the forecast. Despite softness in the auto component of the retail sales report, the rate is only a slight 0.2% decline (-0.8% y/y).

Passenger car sales fueled the overall rate by declining 4.8% (-14.5% y/y) to 5.37 million units. That reversed a modest gain from October. Sales of domestically made cars dropped 5.3% (-13.6% y/y) to 3.95 million units, offsetting the gains in October. Sales of imported passenger cars, down three of the last four months, fell 2.7% (-16.3% y/y) to 1.43 million units.

U.S. light truck sales gained 1.9% in November to 12.12 million units, reversing the decline in October. Sales are nearly at the all-time record high and are 6.8% higher year-over-year.

Sales of domestically-produced light trucks increased 2.2% (4.4% y/y) to 9.71 million units, also reversing the decline in October. Overall, the sales trend is definitely increasing, threatening to set another record high. Sales of imported light trucks gained 0.8% (17.6% y/y) to 2.41 million units, a new record high.

The share of the U.S. vehicle market for trucks reached a record 69.3% in November, a stark improvement from the low of 47.3% all through 2009.

The share of the U.S. vehicle market for imports fell last month at 22.0%, down from the high of 27.6% during 2009. Imports’ share of the passenger car market rose to 26.6%. Imports share of the light truck market was little changed near the cycle high of 19.9%, up from the low of 12.7% in 2014.

[su_table responsive=”yes”]

U.S. Light Weight Vehicle Sales (SAAR, Million Units)

The show talks about the role of government in science and education and how its restrictive nature is potentially a harmful thing and stifles real scientific breakthroughs.

*Bush Worship Continues

*The China Story

*Genetics and Evolution

*Cybernetic Darwinism

*Immortality, then What?

Bumper Music:

Music provided by “Solo Guitar” by Matt LeGroulx in conjunction with Freemusic.org.

Closing Music

http://www.hulkshare.com/praktikos/dark-nights-rise

The money pledged thru Patreon.com will go toward show costs such as advertising, server time, and broadcasting equipment. If we can get enough listeners, we will expand the show to two hours and hire additional staff.

To help our show out, please support us on Patreon: https://www.patreon.com/LibertyNeverSleeps

All bumper music and sound clips are not owned by the show, are commentary, and of educational purposes, or de minimus effect, and not for monetary gain.

No copyright is claimed in any use of such materials and to the extent that material may appear to be infringed, I assert that such alleged infringement is permissible under fair use principles in U.S. copyright laws. If you believe material has been used in an unauthorized manner, please contact the poster.

Businessmen in the Santa hat with big red sack of presents in the City looking through the binocular. Christmas in business, concept illustration. (Photo: AdobeStock)

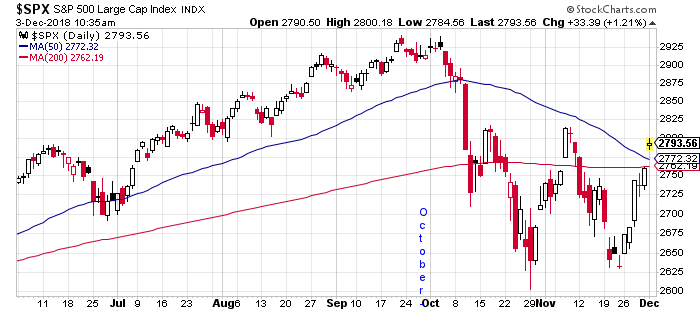

Equity Markets are poised to start the week where they closed out the month of November, on a sharp trajectory higher that could have us testing critical resistance levels during the first few hours of trading.

Clearly, the catalyst for a strong rally across the globe is the thawing of a stalemate on trade talks between the U.S. and China, following a working dinner Saturday evening between their respective trade delegations including President Trump and Chinese President Xi Jinping at the G20 summit in Buenos Aires.

While nothing definitive was agreed to, and admittedly both sides are featuring different points of emphasis, market expectations had been so meager toward any progress that investors are enthusiastically cheering the breakthrough, with gains of nearly +2% in early trading in stock index futures.

The market reaction in China was decidedly positive as stock markets in China and Hong Kong closed out the day with gains ranging from +2.5% to +2.8%.

While a 90 day reprieve leaves much work to be done on both sides, investors are viewing this as much better than the alternative of tariffs being increased from 10% to 25% on over $200 billion of Chinese goods in early 2019.

That being said, if investors sense minimal progress on resolving the difficult issues including Intellectual property rights, and other non-tariff barriers, the enthusiasm could wane quickly as we head into the new year.

If today’s early morning rally holds, the market will be pressing right against the S&P 500; 2810 – 2815 level that proved to be stubborn resistance in both mid October and early November. On both occasions stocks hit that level like a brick wall before turning sharply lower, retreating over 5% within 2 weeks on each occasion.

After stocks put in an almost textbook double bottom, just over 3 weeks apart from October 29 to November 23, my feeling is, we’ll know within a day or two if the 2810 – 2815 level is stubborn resistance for the third time, or if the Santa Claus rally carries through, and into the big gap from the early October sell off.

If the S&P 500 (^SPX) can close above the 2810 – 2815 resistance level with any conviction, it would set the stage for a move higher into year end.

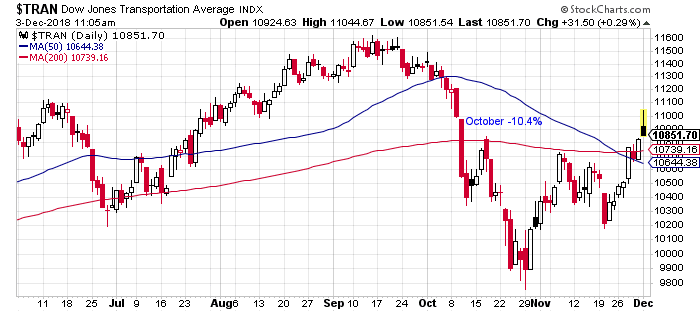

The DJ Transportation Average notably outperformed during November. After over a 10% decline in October, the “death cross” where the 50 day moving average trended below the 200 day MA during the 3rd week of November has so far turned out to be a contra indicator.

The DJTA is poised to close at its highest level since the first week of October, and above both moving averages for the 3rd time in the last 4 days. If the DJ Transports can hold above the 10,800 level it would be very technically positive toward building a base above the reaction highs from mid October and early November.

A couple hours into trading, stocks have given up half their gains from shortly after the opening 30 minutes of trading, but are holding onto gains of 0.75% to 1.0 %. Breadth is still healthy, with advancing issues leading decliners by better than 2 to 1. Retailers and Utilities are 2 of the weaker sectors, with the banks also slightly underperforming.

While some pull back off a sharply higher opening is not alarming, we would certainly view it negatively it the broad market reversed to the downside during the afternoon. Best guess is that is unlikely given the move in global markets overnight, and the market breadth holding predominately green.

Stocks should gain support from the ISM Manufacturing Index (PMI) released this morning, which came in at 59.3, beating consensus of 57.2 and ahead of the October reading of 57.7.

In an environment where there is daily if not hourly chatter over concern of a slowing economy, That’s an Impressive Report.

Men work on a construction site for a luxury apartment complex in downtown Los Angeles, California March 17, 2015. (Photo: Reuters)

Construction spending was estimated at a seasonally adjusted annual rate of $1,308.8 billion for October, a 0.1% (±1.5%)* decline. That’s still 4.9% (±1.6%) above the October 2017 estimate of $1,247.5 billion.

During the first ten months of this year, construction spending amounted to $1,096.4 billion, or 5.1% (±1.2%) higher than the $1,043.6 billion for the same period in 2017.

Private Construction

Spending on private construction was estimated at a seasonally adjusted annual rate of $998.7 billion, a 0.4% (±0.8%)* decline from the revised September estimate of $1,003.0 billion.

Residential construction was at a seasonally adjusted annual rate of $539.0 billion in October, or 0.5% (±1.3%)* below the revised September estimate of $541.7 billion.

Nonresidential construction was at a seasonally adjusted annual rate of $459.7 billion in October, 0.3% (±0.8%)* below the revised September estimate of $461.3 billion.

Public Construction

The estimated seasonally adjusted annual rate of public construction spending was $310.2 billion in October, still 0.8% (±2.6%)* above the revised September estimate of $307.8 billion.

Educational construction was at a seasonally adjusted annual rate of $76.9 billion, or 2.6% (±2.3%)* higher than the revised September estimate of $75.0 billion.

Highway construction came in at a seasonally adjusted annual rate of $94.6 billion, a marginal 0.1% (±6.9%)* decline from the revised September estimate of $94.6 billion.

* The 90 percent confidence interval includes zero. There is insufficient evidence to conclude that the actual change is different from zero.

An American Flag flying in front of a U.S. manufacturing factory. (Photo: AdobeStock)

The Institute for Supply Management (ISM) manufacturing index (PMI) came in at 59.3% in November, easily beating the 57.2% consensus forecast. The forecasts range was 56.0% to 58.3% and the headline is an increase of 1.6 percentage points from the October reading of 57.7%.

“Comments from the panel reflect continued expanding business strength,” Timothy R. Fiore, Chair of the ISM Manufacturing Business Survey Committee, said. “Demand remains strong, with the New Orders Index rebounding to above 60 percent, the Customers’ Inventories Index declining and remaining too low, and the Backlog of Orders Index steady.”

[su_table responsive=”yes”]

Released On 12/3/2018 10:00:00 AM For Nov, 2018

Prior

Consensus

Consensus Range

Actual

ISM Mfg Index – Level

57.7

57.2

56.0 to 58.3

59.3

[/su_table]

The New Orders Index came in at 62.1%, an increase of 4.7 percentage points from the October reading of 57.4%, while the Production Index registered 60.6%, a 0.7 percentage-point increase compared to the October reading of 59.9%.

“The expansion of new export orders was stable and at a recent historical low,” Mr. Fiore added. “However, four of six major industries contributed, down from five in October. Prices pressure continues, but at notably lower levels than in prior periods.”

“The manufacturing community continues to expand, with November adding positively to the three-month rolling PMI® average.”

The Employment Index posted at 58.4%, an increase of 1.6 percentage points from the October reading of 56.8 percent. The Supplier Deliveries Index came in at 62.5%, a 1.3-percentage point decrease from the October reading of 63.8%.

The Inventories Index registered 52.9%, an increase of 2.2 percentage points from the October reading of 50.7%. The Prices Index came in at 60.7%, a 10.9-percentage point decline and indicative of increased raw materials prices for the 33rd month in a row.

Wall Street Campaign Contributions Shift Significantly to Democrats, Against Donald Trump

Graphic concept taking a magnifying glass to Wall Street. (Photo: AdobeStock)

While the securities and finance industry still hedges, Wall Street campaign contributions have shifted significantly over the last two cycles. In 2018, the industry donated more to Democrats than Republicans for the first time in a decade.

The Republican Party, which long had been branded as the party of Big Business, is no longer the top recipient of big money from Wall Street.

In 2018, Democratic candidates and political action committees (PACs) received $57,144,009 in Wall Street campaign contributions, or 62.8% of the total $91,338,283. Republicans received $33,860,538, or 37.2% of total in donations from the securities and finance industry.

That’s the largest disparity between the parties over the 18-year period researched by People’s Pundit Daily. The last time Democrats outpaced Republicans on the Street was in 2008, when George W. Bush relied on his political opposition to pass the Troubled Asset Relief Program, better known as the TARP Bailouts.

Worth noting, less than 1% (0.4%) of the total campaign contributions funded non-major party candidates. While the percentage itself may not sound all that significant, it will be of significant importance later in this series.

The data compiled by the Center for Responsive Politics cover donations during the 2017-2018 election cycle that were released by the Federal Election Commission (FEC) on Tuesday, November 13, 2018. The figures are based on contributions from PACs and individuals who gave ≥ $200.

In the 2018 midterms, the broader sector of finance, insurance and real estate followed a similar pattern. Its firms have given $150,087,616 to Democrats juxtaposed to $128,189,429 to Republicans.

2016 Presidential Election Cycle

In 2016, the $53,237,185 in campaign contributions to Republicans made up 54.5% of the total $97,654,259 for that cycle. That compares to 45%, or $44,417,074 given to Democrats.

Most interesting, congressional campaign contributions do not accurately reflect which horse Wall Street backed at the top of the ticket in 2016.

The securities and finance industry contributed $87,965,257 to Hillary Clinton, a stunning 80.8% of the total $108,807,888 given in two-party contributions.

That compares to the $20,842,631 contributed to then-Republican nominee Donald Trump, a paltry 19.2% of the total.

Unsurprisingly, campaign contributions from the broader finance, insurance and real estate sector also heavily favored the Democratic Party’s nominee. The entire sector gave just $37,873,136 to President Trump, while they contributed a whopping $117,318,552 to Mrs. Clinton.

A comparison of previous cycles certainly appears to strengthen the populism argument, meaning Wall Street’s newfound affliction to the Republican Party looks to be more about President Trump and their electoral expectations than it does about the GOP.

In 2012, the Republican Party enjoyed a significant advantage at both the congressional and presidential level.

Top Five Industries

Industry

Barack Obama

Industry

Mitt Romney

Retired

$53,389,683

Retired

$63,246,113

Lawyers/Law Firms

$27,713,018

Securities & Investment

$23,047,500

Education

$22,631,033

Real Estate

$15,470,102

Health Professionals

$10,573,639

Lawyers/Law Firms

$14,360,501

Civil Servants/Public Officials

$9,006,109

Health Professionals

$13,050,828

The broader finance, insurance and real estate sector backed Mitt Romney over Barack Obama, $61,034,315 to $21,106,073. In fact, the securities and finance industry was the second largest giver to Mr. Romney at $23,047,500, more than the entire sector gave to Mr. Obama.

What should we take from this data?

First, we should reserve at least a certain level of judgement about the impact populism could have on the trend in the mid- to longterm. Wall Street doesn’t like change because it benefits from status quo markets. President Trump’s brand of economic nationalism had not yet taken a hold in the Republican Party in 2016.

But a lot has happened since, and a lot has made them nervous. Nearly $3 billion in lobbying fees spent to ensure the adoption of the Trans-Pacific Partnership (TPP), was wasted.

The renegotiation of the North American Free Trade Agreement (NAFTA) is another trade reform the sector opposes. The same is true of the Street’s concern for the cost of labor to industry without unfettered legal and illegal immigration.

Clearly, the benefits to the U.S. economy from the president’s agenda are offset by the money firms stood and stand to lose from his presidency. The data indicate Wall Street king-makers are less concerned about the national domestic economy than they are about corporate profits.

New Orders, Order Backlogs Hit 4 1/2-Year High; Delivery Times 14 1/2 Years

SUV parts are fabricated in the stamping facility at the General Motors Assembly Plant on June 9, 2015. (Photo: Reuters)

The MNI Chicago Business Barometer (PMI) soared 8 points to an 11-month high of 66.4 in November, crushing the consensus forecast. The consensus was looking for a reading around 58.0 and forecasts ranged from 58.0 to 59.2.

“The MNI Chicago Business Barometer clipped a run of three consecutive declines in emphatic style in November, boosted primarily by resurgent orders – stronger than typically seen at this time of year and enough to push the Barometer to its best level since December,” said Jamie Satchi, Economist at MNI Indicators.

Business activity post its strongest reading this year in November, ending a 3-month losing streak. Gains were broad across all 5 of the Chicago Business Barometer’s subcomponent.

“However, many firms reported seeing the effects of higher China tariffs on their invoices for the first time, and voiced concern that business could be stifled going forward,” Mr. Satchi added.

This month’s result marks 33 consecutive months of growth, or a reading above 50. The headline index has registered above-60 for all but three of the past 15 months.

Today, the show focuses on the Mueller investigation and what they are after by investigating all the people around Trump.

*Big Government is the Problem

*Mueller Has Nothing

*How They Get You

*The Case of Corsi

*A Little On Science

Bumper Music:

Music provided by TRG Music, Livio Amato, A.A Alito and Blue Dot Sessions in conjunction with Freemusic.org.

Closing Music

http://www.hulkshare.com/praktikos/dark-nights-rise

The money pledged thru Patreon.com will go toward show costs such as advertising, server time, and broadcasting equipment. If we can get enough listeners, we will expand the show to two hours and hire additional staff.

To help our show out, please support us on Patreon: https://www.patreon.com/LibertyNeverSleeps

All bumper music and sound clips are not owned by the show, are commentary, and of educational purposes, or de minimus effect, and not for monetary gain.

No copyright is claimed in any use of such materials and to the extent that material may appear to be infringed, I assert that such alleged infringement is permissible under fair use principles in U.S. copyright laws. If you believe material has been used in an unauthorized manner, please contact the poster.

You have %%pigeonMeterAvailable%% free %%pigeonCopyPage%% remaining this month. Get unlimited access and support reader-funded, independent data journalism.