Vice President-elect Mike Pence, R-Ind., and House Majority Leader Kevin McCarthy, R-Calif., attend a press conference with House Speaker Paul Ryan, R-Wis., on Wednesday January 4, 2017.

Vice President-elect Mike Pence said Wednesday at a press conference on Capitol Hill that repealing and replacing ObamaCare will be “first order of business” for House Republicans. President-elect Donald J. Trump plans to sign several executive orders undoing previous orders by President Barack Obama related to ObamaCare on day one. GOP leaders are aiming to have it repealed by Feb. 20th.

“We are 16 days away from business as usual in Washington,” Vice President-elect Pence said. “We are going to be in the promise keeping business.”

The vice president-elect recalled being in Congress when the health care law was passed in 2010 and cited all the broken promises that the president and Democrats had made to the American people.

“Make no mistake about it,” Mr. Pence said. “We’re going to keep our promise to the American people — we’re going to repeal Obamacare and replace it with solutions that lower the cost of health insurance without growing the size of government.”

House Speaker Paul Ryan, R-Wis., who attended the press conference along with House Majority Leader Kevin McCarthy, R-Calif., and House Whip Steve Scalise, R-La., said the plan is to phase out ObamaCare and phase in a replacement to ensure millions aren’t left without coverage.

“So many people have been hurt already,” Speaker Ryan said. “ObamaCare has been a story of broken promise after broken promise after broken promise.”

The press conference only moments before President Obama also arrived on Capitol Hill to meet with Democrats to discuss how to save his signature health care law. Sources tell PPD Mr. Obama told Democrats in Congress “don’t rescue them [Republicans]” by replacing ObamaCare with “something worse.” He told them they should mirror the Tea Party movement on grassroots efforts.

“In two weeks I will no longer be a politician, but I’ll still be a citizen. I envy you so much right now, because I would love to be on the field,” Mr. Obama said, according to a source in the room.

“The reality is that I was here in March of 2010 in another capacity when Obamacare was signed into law,” Vice President-elect Pence told a somewhat hostile group of reporters. “I remember all those promises. We were told that if you like your doctor, you can keep it. Not true.”

Even though President Obama tried to ensure members of his party that they would not lose politically on the issue, the party began to show signs of fracture before the meeting even began. Sen. Joe Manchin, D-W.Va., flat-out questioned the seriousness and wisdom of the meetings held by both the GOP and the president.

“Any type of a meeting that we have that’s not bipartisan is not in the proper scheme of things of starting out the new year,” Sen. Manchin, who skipped the meeting. “It’s just not a good situation for us to be in. So if Mr. Pence is coming up here only to speak to Republicans and President Obama’s coming here only to speak to Democrats, I would be concerned about that. Because I don’t know how you change anything — how do you change anything unless we all come together?”

While CNN reported a lawmaker in the room said the mood among Democrats was “fired up,” he offered no plan for his party to save a deeply unpopular law.

President-elect Donald Trump, Vice-President-elect Mike Pence and House Speaker Paul Ryan wave at a rally Tuesday, Dec. 13, 2016, in West Allis, Wis. (Photo: AP)

I wrote yesterday to praise the Better Way tax plan put forth by House Republicans, but I added a very important caveat: The “destination-based” nature of the revised corporate income tax could be a poison pill for reform.

I listed five concerns about a so-called destination-based cash flow tax (DBCFT), most notably my concerns that it would undermine tax competition (folks on the left think it creates a “race to the bottom” when governments have to compete with each other) and also that it could (because of international trade treaties) be an inadvertent stepping stone for a government-expanding value-added tax.

Brian Garst of the Center for Freedom and Prosperity has just authored a new study on the DBCFT. Here’s his summary description of the tax.

The DBCFT would be a new type of corporate income tax that disallows any deductions for imports while also exempting export-related revenue from taxation. This mercantilist system is based on the same “destination” principle as European value-added taxes, which means that it is explicitly designed to preclude tax competition.

Since CF&P was created to protect and promote tax competition, you won’t be surprised to learn that the DBCFT’s anti-tax competition structure is a primary objection to this new tax.

First, the DBCFT is likely to grow government in the long-run due to its weakening of international tax competition and the loss of its disciplinary impact on political behavior. … Tax competition works because assets are mobile. This provides pressure on politicians to keep rates from climbing too high. When the tax base shifts heavily toward immobile economic activity, such competition is dramatically weakened. This is cited as a benefit of the tax by those seeking higher and more progressive rates. …Alan Auerbach, touts that the DBCFT “alleviates the pressure to reduce the corporate tax rate,” and that it would “alter fundamentally the terms of international tax competition.” This raises the obvious question—would those businesses and economists that favor the DBCFT at a 20% rate be so supportive at a higher rate?

Brian also shares my concern that the plan may morph into a VAT if the WTO ultimately decides that is violates trade rules.

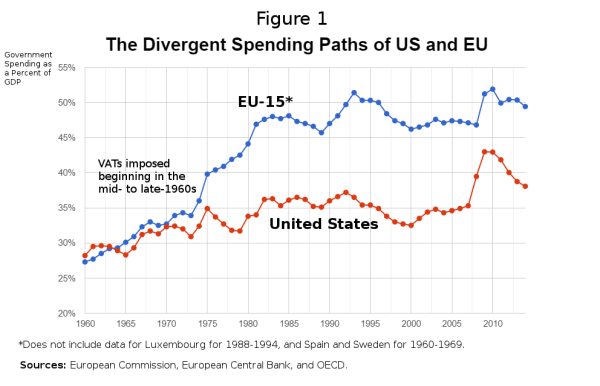

Second, the DBCFT almost certainly violates World Trade Organization commitments. …Unfortunately, it is quite possible that lawmakers will try to “fix” the tax by making it into an actual value-added tax rather than something that is merely based on the same anti-tax competition principles as European-style VATs. …the close similarity of the VAT and the DBCFT is worrisome… Before VATs were widely adopted, European nations featured similar levels of government spending as the United States… Feeding at least in part off the easy revenue generate by their VATs, European nations grew much more drastically over the last half century than the United States and now feature higher burdens of government spending. The lack of a VAT-like revenue engine in the U.S. constrained efforts to put the United States on a similar trajectory as European nations.

And if you’re wondering why a VAT would be a bad idea, here’s a chart from Brian’s paper showing how the burden of government spending in Europe increased once that tax was imposed.

In the new report, Brian elaborates on the downsides of a VAT.

If the DBCFT turns into a subtraction-method VAT, its costs would be further hidden from taxpayers. Workers would not easily understand that their employers were paying a big VAT withholding tax (in addition to withholding for income tax). This makes it easier for politicians to raise rates in the future. …Keep in mind that European nations have corporate income tax systems in addition to their onerous VAT regimes.

And he points out that those who support the DBCFT for protectionist reasons will be disappointed at the final outcome.

…if other nations were to follow suit and adopt a destination-based system as proponents suggest, it will mean more taxes on U.S. exports. Due to the resulting decline in competitive downward pressure on tax rates, the long-run result would be higher tax burdens across the board and a worse global economic environment.

Brian concludes with some advice for Republicans.

Lawmakers should always consider what is likely to happen once the other side eventually returns to power, especially when they embark upon politically risky endeavors… In this case, left-leaning politicians would see the DBCFT not as something to be undone, but as a jumping off point for new and higher taxes. A highly probable outcome is that the United States’ corporate tax environment becomes more like that of Europe, consisting of both consumption and income taxes. The long-run consequences will thus be the opposite of what today’s lawmakers hope to achieve. Instead of a less destructive tax code, the eventual result could be bigger government, higher taxes, and slower economic growth.

Amen.

My concern with the DBCFT is partly based on theoretical objections, but what really motivates me is that I don’t want to accidentally or inadvertently help statists expand the size and scope of government. And that will happen if we undermine tax competition and/or set in motion events that could lead to a value-added tax.

Let’s close with three hopefully helpful observations.

Helpful Reminder #1: Congressional supporters want a destination-based system as a “pay for” to help finance pro-growth tax reforms, but they should keep in mind that leftists want a destination-based system for bad reasons.

Based on dozens of conversations, I think it’s fair to say that the supporters of the Better Way plan don’t have strong feelings for destination-based taxation as an economic principle. Instead, they simply chose that approach because it is projected to generate $1.2 trillion of revenue and they want to use that money to “pay for” the good tax cuts in the overall plan.

That’s a legitimate choice. But they also should keep in mind why other people prefer that approach. Folks on the left want a destination-based tax system because they don’t like tax competition. They understand that tax competition restrains the ability of governments to over-tax and over-spend. Governments in Europe chose destination-based value-added taxes to prevent consumers from being able to buy goods and services where VAT rates are lower. In other words, to neuter tax competition.

Some state governments with high sales taxes in the United States are pushing a destination-based system for sales taxes because they want to hinder consumers from buying goods and services from states with low (or no) sales taxes. Again, their goal is to cripple tax competition.

Something else to keep in mind is that leftist supporters of the DBCFT also presumably see the plan as being a big step toward achieving a value-added tax, which they support as the most effective way of enabling bigger government in the United States.

Helpful Reminder #2: Choosing the right tax base (i.e., taxing income only one time, otherwise known as a consumption-base system) does not require choosing a destination-based approach.

The proponents of the Better Way plan want a “consumption-base” tax. This is a worthy goal. After all, that principle means a system where economic activity is taxed only one time. But that choice is completely independent of the decision whether the tax system should be “origin-based” or “destination-based.”

The gold standard of tax reform has always been the Hall-Rabushka flat tax, which is a consumption-base tax because there is no double taxation of income that is saved and invested. It also is an “origin-based” tax because economic activity is taxed (only one time!) where income is earned rather than where income is consumed.

The bottom line is that you can have the right tax base with either an origin-based system or a destination-based system.

Helpful Reminder #3: The good reforms of the Better Way plan can be achieved without the downside risks of a destination-based tax system.

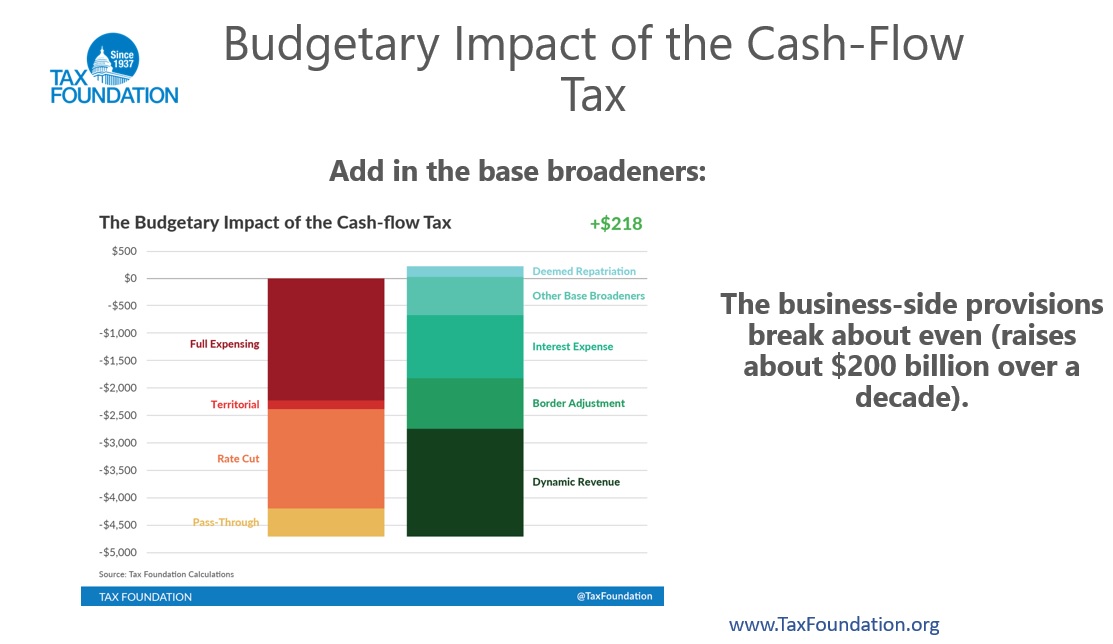

The Tax Foundation, even in rare instances when I disagree with its conclusions, always does very good work. And they are the go-to place for estimates of how policy changes will affect tax receipts and the economy. Here is a chart with their estimates of the revenue impact of various changes to business taxation in the Better Way plan. As you can see, the switch to a destination-based system (“border adjustment”) pulls in about $1.2 trillion over 10 years. And you can also see all the good reforms (expensing, rate reduction, etc) that are being financed with the various “pay fors” in the plan.

I am constantly asked how the numbers can work if “border adjustment” is removed from the plan. That’s a very fair question.

But there are lots of potential answers, including:

Make a virtue out of necessity by reducing government revenue by $1.2 trillion.

Reduce the growth of government spending to generate offsetting savings.

Find other “pay fors” in the tax code (my first choice would be the healthcare exclusion).

Reduce the size of the tax cuts in the Better Way plan by $1.2 trillion.

I’m not pretending that any of these options are politically easy. If they were, the drafters of the Better Way plan probably would have picked them already. But I am suggesting that any of those options would be better than adopting a destination-based system for business taxation.

Ultimately, the debate over the DBCFT is about how different people assess political risks. House Republicans advocating the plan want good things, and they obviously think the downside risks in the future are outweighed by the ability to finance a larger level of good tax reforms today. Skeptics appreciate that those proponents want good policy, but we worry about the long-run consequences of changes that may (especially when the left sooner or late regains control) enable bigger government.

Christian persecution in the Middle East and worldwide is on the rise. Coptic Christians in Egypt worship (above), but are becoming all but extinct at the hands of Islamists. (Photo: AP)

Christians were the most persecuted religious group in the world in 2016, according to a new study conducted by the Center for Studies on New Religions (CESNUR). The group, which is based in Turin, Italy, found that 90,000 Christians were killed last year, of which 30% were killed by Islamists.

The remaining 60,000 persecuted and murdered Christians were killed largely by secular leftist-run state and non-state actors around the world, including but not limited to the communist regime in North Korea.

Georgetown University describes CESNUR as “an independent international network that engages in scholarly research and provides accurate information to the public on new religious movements, always protecting religious freedom while acknowledging the criminal nature of certain cult activities.”

House Speaker Paul Ryan, R-Wis., administers the House oath of office to Rep. Kevin Brady, R-Texas, during a mock swearing in ceremony on Capitol Hill, Tuesday, Jan. 3, 2017, in Washington. (Photo: AP)

The Republicans in the House of Representatives, led by Ways & Means Chairman Kevin Brady and Speaker Paul Ryan, have proposed a “Better Way” tax plan that has many very desirable features.

And there are many other provisions that would reduce penalties on work, saving, investment, and entrepreneurship. No, it’s not quite a flat tax, which is the gold standard of tax reform, but it is a very pro-growth initiative worthy of praise.

That being said, there is a feature of the plan that merits closer inspection. The plan would radically change the structure of business taxation by imposing a 20 percent tax on all imports and providing a special exemption for all export-related income. This approach, known as “border adjustability,” is part of the plan to create a “destination-based cash flow tax” (DBCFT).

When I spoke about the Better Way plan at the Heritage Foundation last month, I highlighted the good features of the plan in the first few minutes of my brief remarks, but raised my concerns about the DBCFT in my final few minutes.

Allow me to elaborate on those comments with five specific worries about the proposal.

Concern #1: Is the DBCFT protectionist?

It certainly sounds protectionist. Here’s how the Financial Timesdescribed the plan.

The border tax adjustment would work by denying US companies their current ability to deduct import costs from their taxable income, meaning companies selling imported products would effectively be taxed on the full value of the sale rather than just the profit. Export revenues, meanwhile, would be excluded from company tax bases, giving net exporters the equivalent of a subsidy that would make them big beneficiaries of the change.

Charles Lane of the Washington Postexplains how it works.

…the DBCFT would impose a flat 20 percent tax only on earnings from sales of output consumed within the United States… It gets complicated, but the upshot is that the cost of imported supplies would no longer be deductible from taxable income, while all revenue from exports would be. This would be a huge incentive to import less and export more, significant change indeed for an economy deeply dependent on global supply chains.

That certainly sounds protectionist as well. A tax on imports and a special exemption for exports.

But proponents say there’s no protectionism because the tax is neutral if the benchmark is where products are consumed rather than where income is earned. Moreover, they claim exchange rates will adjust to offset the impact of the tax changes. Here’s how Lane explains the issue.

…the greenback would have to rise 25 percent to offset what would be a new 20 percent tax on imported inputs — propelling the U.S. currency to its highest level on record. The international consequences of that are unforeseeable, but unlikely to be totally benign for everyone. Bear in mind that many other countries — China comes to mind — can and will manipulate exchange rates to protect their own short-term interests.

For what it’s worth, I accept the argument that the dollar will rise in value, thus blunting the protectionist impact of border adjustability. It would remain to be seen, though, how quickly or how completely the value of the dollar would change.

Concern #2: Is the DBCFT compliant with WTO obligations?

The United States is part of the World Trade Organization (WTO) and we have ratified various agreements designed to liberalize world trade. This is great for the global economy, but it might not be good news for the Better Way plan because WTO rules only allow border adjustability for indirect taxes like a credit-invoice value-added tax. The DBCFT, by contrast, is a version of a corporate income tax, which is a direct tax.

The column by Charles Lane explains one of the specific problems.

Trading partners could also challenge the GOP plan as a discriminatory subsidy at the World Trade Organization. That’s because it includes a deduction for wages paid by U.S.-located firms, importers and exporters alike — a break that would obviously not be available to competitors abroad.

Advocates argue that the DBCFT is a consumption-base tax, like a VAT. And since credit-invoice VATs are border adjustable, they assert their plan also should get the same treatment. But the WTO rules say that only “indirect” taxes are eligible for border adjustability. The New York Timesreports that the WTO therefore would almost surely reject the plan.

Michael Graetz, a tax expert at the Columbia Law School, said he doubted that argument would prevail in Geneva. “W.T.O. lawyers do not take the view that things that look the same economically are acceptable,” Mr. Graetz said.

A story in the Wall Street Journal considers the potential for an adverse ruling from the World Trade Organization.

Even though it’s economically similar to, and probably better than, the value-added taxes (VATs) many other countries use, it may be illegal under World Trade Organization rules. An international clash over taxes is something the world can ill afford when protectionist sentiment is already running high. …The controversy is over whether border adjustability discriminates against trade partners. …the WTO operates not according to economics but trade treaties, which generally treat tax exemptions on exports as illegal unless they are consumption taxes, such as the VAT. …the U.S. has lost similar disputes before. In 1971 it introduced a tax break for exporters that, despite several revamps, the WTO ruled illegal in 2002.

And a Washington Posteditorial is similarly concerned.

Republicans are going to have to figure out how to make such a huge de facto shift in the U.S. tax treatment of imports compliant with international trade law. In its current iteration, the proposal would allow corporations to deduct the costs of wages paid within this country — a nice reward for hiring Americans and paying them well, which for complex reasons could be construed as a discriminatory subsidy under existing World Trade Organization doctrine.

Concern #3: Is the DBCFT a stepping stone to a VAT?

If the plan is adopted, it will be challenged. And if it is challenged, it presumably will be rejected by the WTO. At that point, we would be in uncharted territory.

Would that force the folks in Washington to entirely rewrite the tax system? Would they be more surgical and just repeal border adjustability? Would they ignore the WTO, which would give other nations the right to impose tariffs on American exports?

One worrisome option is that they might simply turn the DBCFT into a subtraction-method value-added tax (VAT) by tweaking the law so that employers no longer could deduct expenses for labor compensation. This change would be seen as more likely to get approval from the WTO since credit-invoice VATs are border adjustable.

This possibility is already being discussed. The Wall Street Journal story about the WTO issue points out that there is a relatively simple way of making the DBCFT fit within America’s trade obligations, and that’s to turn it into a value-added tax.

One way to avoid such a confrontation would be to revise the cash flow tax to make it a de facto VAT.

One tax initiative that should be strangled before it sees the light of day is to give a tax rebate to exporters and to impose taxes on imports. …It’s a bad idea. Why do we want to make American consumers pay more for products while subsidizing foreign buyers? It also could put us on the slippery slope to our own VAT.

And that’s not a slope we want to be on. Unless the income tax is fully repealed (sadly not an option), a VAT would be a recipe for turning America into a European-style welfare state.

Concern #4: Does the DBCFT undermine tax competition and give politicians more ability to increase tax burdens?

Alan Auerbach, an academic from California who previously was an adviser for John Kerry and also worked at the Joint Committee on Taxation when Democrats controlled Capitol Hill, is the main advocate of a DBCFT (the New York Times wrote that he is the “principal intellectual champion” of the idea).

He wrote a paper several years ago for the Center for American Progress, a hard-left group closely associated with Hillary Clinton. Auerbach explicitly argued that this new tax scheme is good because politicians no longer would feel any pressure to lower tax rates.

This…alternative treatment of international transactions that would relieve the international pressure to reduce rates while attracting foreign business activity to the United States. It addresses concerns about the effect of rising international competition for multinational business operations on the sustainability of the current corporate tax system. With rising international capital flows, multinational corporations, and cross-border investment, countries’ tax rates and tax structures are of increasing importance. Indeed, part of the explanation for declining corporate tax rates abroad is competition among countries for business activity. …my proposed reforms…builds on the [Obama] Administration’s approach…and alleviates the pressure to reduce the corporate tax rate.

This is very troubling. Tax competition is a very valuable liberalizing force in the world economy. It partially offsets the public choice pressures on politicians to over-tax and over-spend. If governments no longer had to worry that taxable activity could escape across national borders, they would boost tax rates and engage in more class warfare.

Concern #5: Does the DBCFT create needless conflict and division among supporters of tax reform?

As I pointed out in my remarks at the Heritage Foundation, there’s normally near-unanimous support from the business community for pro-growth tax reforms.

That’s not the case with the DBCFT.

The Washington Examiner reports on the divisions in the business community.

Major retailers are skeptical of the House Republican plan to revamp the tax code, fearing that the GOP call to border-adjust corporate taxes could harm them even if they win a significant cut to their tax rate. As a result, retailers, oil refiners and other industries that import goods to sell in the U.S. could provide a major obstacle to the Republican effort to reform taxes. …The effect of the border adjustment, retailers fear, would be that the goods they import to sell to consumers would face a 20 percent mark-up, one that would force retailers like Walmart, the Home Depot and Sears…to raise prices and lose customers.

A story from CNBC highlights why retailers are so concerned.

…retailers are nervous. Very nervous. …About 95 percent of clothing and shoes sold in the U.S. are manufactured overseas, which means imports make up a vast majority of many U.S. retailers’ merchandise. …If the GOP plan were adopted as it’s currently laid out, Gap pays 20 percent corporate tax on the $5 profit from the sweater, or $1. Plus, 20 percent tax on the $80 cost it paid for that sweater from the overseas supplier, or $16. That means the tax goes from $1.75 to $17 for that sweater, more than three times the profit on that sweater. Talk about a hit to margins. …Retailers certainly aren’t taking a lot of comfort in the economic theory of dollar appreciation. …the tax reform plan will dilute specialty retailers’ earnings by an average of 132 percent. …Athletic manufacturers could take a 40 percent earnings hit… Gap, Carter’s , Urban Outfitters , Fossil and Under Armour are most at risk under the plan.

And here’s another article from the Washington Examiner that explains why folks in the energy industry are concerned.

…the border adjustment would raise costs for refiners that import oil. In turn, that could raise prices for consumers. The border adjustment would amount to a $10-a-barrel tax on imported crude oil, raising costs for drivers buying gasoline by up to 25 cents a gallon, the energy analyst group PIRA Energy Group warned this week. The report warned of a “potential huge impact across the petroleum industry,” even while noting that the tax reform plan faces many obstacles to passage.

Concern #6: What happens when other nations adopt their versions of a DBCFT?

Advocates of the DBCFT plausibly argue that if the WTO somehow approves their plan, then other nations will almost certainly copy the new American system.

But is also has negative implications for the fight to protect America from a VAT. The main selling point for advocates of the DBCFT is that we need a border-adjustable tax to offset the supposed advantage that other nations have because of border-adjustable VATs (both Paul Krugman and I agree that this is nonsense, but it still manages to be persuasive for some people).

So what happens when other nations turn their corporate income taxes into DBCFTs, which presumably will happen? We’re than back where we started and misguided people will say we need our own VAT to balance out the VATs in other nations.

The bottom line is that a DBCFT is not the answer to America’s wretched business tax system. There are simply too many risks associated with this proposal. I’ll elaborate tomorrow in Part II and also explain some good ways of pursuing tax reform without a DBCFT.

Israeli Prime Minister Benjamin Netanyahu, center, arrives for a weekly cabinet meeting, in Jerusalem, Sunday, Jan. 1, 2017. (Photo: AP)

Republican Senators Ted Cruz (TX), Marco Rubio and Dean Heller (Nev.), introduced a bill Tuesday that would move the U.S. embassy in Israel from Tel Aviv to Jerusalem. The Jerusalem Embassy and Recognition Act would fulfill a 21-year old promise by the U.S. to Israel and comes just 12 days after the Obama administration abstained from a key U.N. Security Council vote condemning their ally for settlements in the West Bank.

The three Republicans introduced the bill in the first session of the 115th Congress, which began Tuesday. It recognizes Jerusalem as the capital of Israel and mandates the relocation of the U.S. embassy to Jerusalem in order for it to “remain an undivided city in which the rights of every ethnic and religious group are protected as they have been by Israel since 1967.”

“Jerusalem is the eternal and undivided capital of Israel,” Sen. Cruz said in a statement. “Unfortunately, the Obama administration’s vendetta against the Jewish state has been so vicious that to even utter this simple truth – let alone the reality that Jerusalem is the appropriate venue for the American embassy in Israel- is shocking in some circles.”

Sen. Rubio, who slammed the Obama administration as anti-Israel following the U.N. vote, also released a statement saying “it is time for Congress and the President-elect to eliminate the loophole that has allowed presidents in both parties to ignore U.S. law and delay our embassy’s rightful relocation to Jerusalem for over two decades.”

In fact, Congress in 1995 already passed The Jerusalem Embassy and Relocation Act, which recognized Jerusalem as the capital of Israel by moving the U.S. Embassy from Tel Aviv to Jerusalem. However, the promise has not been fulfilled and the law has not been followed for 21 years.

President-elect Donald J. Trump has vowed his administration would move the U.S. Embassy from Tel Aviv to Jerusalem and nominated David Friedman for Ambassador to Israel. Mr. Friedman, a New York bankruptcy lawyer, also advocates for the relocation.

“It honors an important promise America made more than two decades ago but has yet to fulfill,” Sen. Heller said.

Former U.N. Ambassador John Bolton, who was in the running for secretary of state, said the move would not be as difficult as critics claim. He suggested temporarily making the consulate in Jerusalem the embassy, with an official diplomatic building to be constructed at a later date.

[newsletter_signup_form id=3]

“There is an international significance and there is a political significance here,” Mr. Bolton told Fox News. “Trump will distinguish himself from other politicians: he made the commitment, and I think he will actually follow through with it.”

Now, the Republican senators have sought to add teeth to the law and force the executive branch to enforce it by restricting funding for the U.S. State Department during fiscal year 2017. Under the “Embassy Security, Construction, and Maintenance” section, the bill prohibits appropriation of more than 50% of funding to the State Department until the secretary reports that the Embassy in Jerusalem has officially opened.

“It is finally time to cut through the double-speak and broken promises and do what Congress said we should do in 1995: formally move our embassy to the capital of our great ally Israel,” Sen. Cruz said.

Sen. Charles Grassley, R-Iowa, Chairman of the Senate Judiciary Committee, meets with Attorney General nominee Sen. Jeff Sessions, R-Ala., on Tuesday, Nov. 29, 2016 in Washington. (Photo: AP)

Sen. Jeff Sessions, R-Ala., President-elect Donald J. Trump’s nominee for Attorney General, is getting an outpouring of support as he comes under organized fire by Democrats. The former federal and state prosecutor is scheduled to appear for confirmation hearings before the Senate Judiciary Committee on Jan. 10 and 11.

Sen. Tom Cotton, R-Ark., who met with the AG nominee on Tuesday to discuss the hearings, defended Sen. Sessions even as the NAACP occupied his office.

“Jeff Sessions is one of the most qualified nominees for Attorney General in history and will be an exemplary leader at the Justice Department,” Sen. Cotton said in a statement released following the meeting. “I have come to know Jeff well in our time in the Senate, and I have seen his integrity up close. He will be a steadfast defender of the Constitution and the rule of law. And he is committed to securing our borders and fixing our broken immigration system. I look forward to supporting his nomination.”

NAACP President Cornell William Brooks and other leftwing activists are staging a sit-in at Sen. Sessions’ office in Mobile, Alabama, to protest his nomination. During a press conference, the group said they will not leave until Sessions withdraws his nomination or the protesters are arrested.

The NAACP and other leftwing groups point to Sessions’ nomination for a federal judgeship in 1986 that failed after allegations surfaced that he made racist comments while he was serving as a U.S. attorney in Alabama. A former colleague claimed he at the time called the NAACP “un-American.”

Benard Simelton, president of the Alabama State Conference of the NAACP, said in a statement that Sessions has “been a threat to desegregation and the Voting Rights Act and remains a threat to all of our civil rights, including the right to live without the fear of police brutality.”

But Ken Blackwell, the former Ohio secretary of state and an African American, wrote in an op-ed that “freedom of speech has come under fire as well.” He called on senators to confirm his nomination without delay.

“Of course, Democrats fear government rooted in law, but they can’t admit that in public. So they are resorting to their usual smear tactics, branding Sessions as a racist,” Mr. Blackwell said. “What really scares Sessions’ opponents is that the former U.S. Attorney and Alabama Attorney General really knows the issues and what is necessary to fix the DOJ, a department badly politicized by the Obama administration. Sessions also knows where the bodies are buried there, including the ones that have been moved.—and how often they vote.”

Columnist Quin Hillyer, who has followed Sessions’ career, dismissed the criticism and charges of racism.

“Mr. Sessions has now served 20 years in the Senate,” Hillyer said. “No racist could keep bigotry closeted for so long.”

Jonathan Thompson, the Executive Director of the National Sheriff’s Association, penned an op-ed in The Hill slamming the lawlessness allowed to fester under the Obama administration and praising Sen. Sessions.

“The Senate must confirm Sen. Sessions because law enforcement and the citizens they protect need his expertise, dedication and honor at the Justice Department,” he wrote. “The nation’s sheriffs and deputies know Sen. Sessions will support them because throughout his career he has been a crime fighter who seeks justice fairly.”

From left to right: Fox News debate moderators Chris Wallace, Megyn Kelly, and Bret Baier. (Photo: AP)

Megyn Kelly, host of the show “The Kelly File,” will leave Fox News later this year to join NBC News, an outlet hostile to President-elect Donald J. Trump. Kelly, who has frequently criticized NBC News and others as not being “Fair and Balanced,” grew in popularity among mainstream media elites for her public feud with the then-Republican frontrunner and New York businessman.

She will join NBC News as host of a daytime news program and anchor of a Sunday night news show, three sources with knowledge of the matter told CNNMoney.

“Megyn is an exceptional journalist and news anchor, who has had an extraordinary career,” NBCUniversal News Group chairman Andy Lack said in an email to staff. “She’s demonstrated tremendous skill and poise, and we’re lucky to have her.”

While the development appears to be a major boon for NBC and blow to Fox News, Kelly’s feud has also resulted in major damage to Fox News’ brand. In August, 2015, FOX News hosted the first Republican presidential debate and boasted their highest ratings ever. But it sparked the controversy between Ms. Kelly and Mr. Trump, which viewers frowned upon.

Their brand among Republicans tanked and, according to the YouGov BrandIndex survey, their image among the general public overall also took a dive, fell to par with CNN and the trend lines were moving in the wrong direction.

Still, sources with knowledge of the matter said that Fox News has offered Kelly an annual salary of more than $20 million to stay at the network, matching the salary of her colleague and rival, Bill O’Reilly. She and her representatives also held talks with CNN, ABC and other outlets before deciding on NBC, an outlet revealed in the WikiLeaks dumps to be more than a little corrupt and bias.

NBC News has not disclosed the terms of Kelly’s new contract.

Republican vice presidential nominee Mike Pence (L-R), Representative Kevin McCarthy (R-CA) and U.S. House Speaker Paul Ryan (R-WI) laugh when a reporter Ryan called on began to ask Pence a question about his criticism of Donald Trump, during a joint news conference. (PHOTO: REUTERS)

Facing criticism from President-elect Donald J. Trump, House Republicans abandoned a proposal aiming to make controversial changes to the Office of Congressional Ethics. President-elect Trump criticized the plan, as well as others, as the 115th Congress opens on a contentious note.

With all that Congress has to work on, do they really have to make the weakening of the Independent Ethics Watchdog, as unfair as it

House Speaker Paul Ryan, R-Wis., as well as Majority Leader Kevin McCarthy, R-Calif., were opposed to the plan, which would’ve placed the independent ethics office under the authority of a congressional committee. Nevertheless, they intended to go along with the changes.

Donald J. Trump holds a rally in Michigan in March, 2016.

DEVELOPING: Ford Motor Company (NYSE:F) announced it has cancelled plans to build a $1.6 billion factory in Mexico and will instead invest millions in Michigan. CEO Mark Fields said the policies President-elect Donald J. Trump “and the new Congress have indicated they will pursue” were key to the company’s decision to invest $700 million in and create 700 direct new jobs at the Flat Rock Assembly Plant.

The company was frequently criticized by President-elect Trump during the campaign for investing outside the country, particularly in Mexico. Hammering home his economic message on trade and manufacturing, the New York businessman became the first Republican nominee to carry the state of Michigan since 1988.

United Auto Workers Vice President Jimmy Settles reacted in response to Ford’s decision.

“I am thrilled that we have been able to secure additional UAW-Ford jobs for American workers,” Mr. Settles said. “The men and women of Flat Rock Assembly have shown a great commitment to manufacturing quality products, and we look forward to their continued success with a new generation of high-tech vehicles.”

With the automaker abandoning plans to build a plant in San Luis Potosi, Mexico, they make way for two new iconic products–the Ford Mustang and Lincoln Continental–at the Michigan Assembly Plant in Wayne, where Focus is manufactured today. The decision safeguards approximately 3,500 U.S. jobs. While Ford will still build its next-generation Focus in Hermosillo, Mexico, the location is at an existing plan to improve company profitability.

“As more and more consumers around the world become interested in electrified vehicles, Ford is committed to being a leader in providing consumers with a broad range of electrified vehicles, services and solutions that make people’s lives better,” said Mark Fields, Ford president and CEO. “Our investments and expanding lineup reflect our view that global offerings of electrified vehicles will exceed gasoline-powered vehicles within the next 15 years.”

Instead of driving jobs and wealth away, AMERICA will become the world's great magnet for INNOVATION & JOB CREATION.https://t.co/siXrptsOrt

Ford stock was up 3.21%, or 0.39 to $12.51 a share on the heels of the announcement. The move indicates the company expects the policy of the incoming Trump administration to be more business friendly, as do most other companies in most other sectors. Ford is already America’s top-selling plug-in hybrid brand and second in overall U.S. electrified vehicle sales, but now aims to create a factory capable of producing high-tech electrified and autonomous vehicles.

“Innovative services can be as important to customers as the electrified vehicles themselves,” said Hau Thai-Tang, group vice president of Purchasing and Ford’s EV champion. “We are investing in solutions to help private customers as well as commercial fleet owners seamlessly incorporate these new vehicles and technologies into their lives.”

The Institute for Supply Management’s Manufacturing Report On Business Survey. (Photo: REUTERS)

The ISM Report on Business, the Institute for Supply Management’s gauge of factory activity nationwide, rose to 54.7 in December from 53.2 in November. Economists expected an increase to 53.6 for the month.

Readings above 50 point to expansion, while those below indicate contraction.

“The New Orders Index registered 60.2 percent, an increase of 7.2 percentage points from the November reading of 53 percent,” Bradley J. Holcomb, chair of the Institute for Supply Management Manufacturing Business Survey Committee. “The Production Index registered 60.3 percent, 4.3 percentage points higher than the November reading of 56 percent.”

Of the 18 manufacturing industries, 11 are reporting growth in December in the following order: Petroleum & Coal Products; Primary Metals; Miscellaneous Manufacturing; Food, Beverage & Tobacco Products; Apparel, Leather & Allied Products; Paper Products; Machinery; Electrical Equipment, Appliances & Components; Computer & Electronic Products; Fabricated Metal Products; and Chemical Products.

“The Employment Index registered 53.1 percent, an increase of 0.8 percentage point from the November reading of 52.3 percent,” Mr. Holcomb added. “Inventories of raw materials registered 47 percent, a decrease of 2 percentage points from the November reading of 49 percent.”

The six industries reporting contraction in December — listed in order — are: Plastics & Rubber Products; Furniture & Related Products; Printing & Related Support Activities; Textile Mills; Nonmetallic Mineral Products; and Transportation Equipment.

MANUFACTURING AT A GLANCE

December 2016

Index

Series Index

Dec

Series Index

Nov

Percentage

Point

Change

Direction

Rate of Change

Trend* (Months)

PMI®

54.7

53.2

+1.5

Growing

Faster

4

New Orders

60.2

53.0

+7.2

Growing

Faster

4

Production

60.3

56.0

+4.3

Growing

Faster

4

Employment

53.1

52.3

+0.8

Growing

Faster

3

Supplier Deliveries

52.9

55.7

-2.8

Slowing

Slower

8

Inventories

47.0

49.0

-2.0

Contracting

Faster

18

Customers’ Inventories

49.0

49.0

0.0

Too Low

Same

3

Prices

65.5

54.5

+11.0

Increasing

Faster

10

Backlog of Orders

49.0

49.0

0.0

Contracting

Same

6

New Export Orders

56.0

52.0

+4.0

Growing

Faster

10

Imports

50.5

50.5

0.0

Growing

Same

3

OVERALL ECONOMY

Manufacturing Sector

Growing

Faster

91

Growing

Faster

4

Manufacturing ISM® Report On Business® data is seasonally adjusted for the New Orders, Production, Employment and Supplier Deliveries Indexes.

You have %%pigeonMeterAvailable%% free %%pigeonCopyPage%% remaining this month. Get unlimited access and support reader-funded, independent data journalism.