U.S. jobless claims graph on a tablet screen. (Photo: AdobeStock)

Initial jobless claims fell 8,000 to a seasonally adjusted 221,000 for the week ending June 29, the Labor Department reported. The 4-week moving average ticked slightly higher by 500 to 222,250.

Indicator

Prior

Prior Revised

Consensus Forecast

Forecast Range

Result

Initial Jobless Claims

227 K

229 K

220 K

217 K to 225 K

221 K

The advance seasonally adjusted insured unemployment rate remained unchanged at 1.2% for the week ending June 2. The advance number for seasonally adjusted insured unemployment declined by 8,000 during the week ending June 22 to 1,686,000.

No state was triggered “on” the Extended Benefits program during the week ending June 15.

The highest insured unemployment rates in the week ending June 15 were in Puerto Rico (2.1), Alaska (1.9), New Jersey (1.9), California (1.8), Connecticut (1.8), Pennsylvania (1.7), Illinois (1.5), Massachusetts (1.4), and Rhode Island (1.4).

The largest increases in initial claims for the week ending June 22 were in California (+5,643), New Jersey (+5,580), Massachusetts (+4,660), Connecticut (+3,719), and Maryland (+1,742), while the largest decreases were in Pennsylvania (-947), Illinois (-738), Puerto Rico (-640), Texas (-587), and New York (-504).

Employment Revised Higher for May: 27,000 to 41,000

Man reading newspaper with the headline Job Market. (Photo: AdobeStock)

The ADP National Employment Report finds the U.S. private sector added 102,000 jobs in June, less than the forecast. The total of jobs added for May was revised up from 27,000 to 41,000.

Indicator

Prior

Prior Revised

Consensus Forecast

Forecast Range

Result

ADP

27,000

41,000

140,000

130,000 to 190,000

102,000

“Job growth started to show signs of a slowdown,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “While large businesses continue to do well, small businesses are struggling as they compete with the ongoing tight labor market. The goods producing sector continues to show weakness. Among services, leisure and hospitality’s weakness could be a reflection of consumer confidence.”

Small businesses (1-49 employees) lost 23,000, while medium businesses (50-499) added 60,000 and large (500+) added 65,000.

“The job market continues to throttle back. Job growth has slowed sharply in recent months, as businesses have turned more cautious in their hiring,” Mark Zandi, chief economist of Moody’s Analytics, said. “Small businesses are the most nervous, especially in the construction sector and at bricks-and-mortar retailers.”

U.S. Navy SEAL Chief Edward Gallagher, left, and his wife, Andrea Gallagher arrive at military court Monday July 2, 2019.

U.S. Navy SEAL Chief Edward “Eddie” Gallagher was found not guilty on nearly all charges, including murder and attempted murder. A jury cleared the decorated team leader in the killing of an Islamic State member in Iraq.

Prosecutors alleged he killed an Islamic State militant being treated by medics. The defense argued Chief Gallagher was an “old-school, hard-charging warrior” targeted by “millennial” SEALs who harbored “personal animosity” toward him.

He was charged with seven counts including premeditated murder, willfully discharging a firearm to endanger human life, posing for a photo with a casualty, retaliation against members of his platoon for reporting his alleged actions, obstruction of justice, and the attempted murders of two noncombatants.

He was found guilty of only posing for a photo with a human casualty.

The case against Chief Gallagher was rocked when a key witness for the prosecution testified he caused the prisoner’s death, himself. Special Operator First Class Corey Scott, a U.S. Navy SEAL medic, initially claimed he saw Chief Gallagher pull out his knife and stab the prisoner under his collar bone.

But under oath and on cross-examination, he said he never saw any blood after the stabbing, He dropped a bombshell when he admitted to suffocating the prisoner in what he referred to as an act of mercy.

First Class Corey Scott said that he had held his thumb over his trachea tube to spare the prisoner from torture at the hands of Iraqi forces.

While he initially did not admit to killing the prisoner in previous interviews, he said being granted immunity allowed him to come forward. The prosecutor called him a liar and threatened a perjury charge.

This is not quite as pronounced as Argentina’s drop in the rankings for per-capita GDP, but it’s definitely a sign that something’s gone wrong in the Land of the Rising Sun.

On Liberty Never Sleeps, Tom argues the faces of Democrats have changed, but the lines of nonsense people have been buying for at least 50 years, have not.

The money pledged thru Patreon.com will go toward show costs such as advertising, server time, and broadcasting equipment. If we can get enough listeners, we will expand the show to two hours and hire additional staff.

To help our show out, please support us on Patreon.

All bumper music and sound clips are not owned by the show, are commentary, and of educational purposes, or de minimus effect, and not for monetary gain.

No copyright is claimed in any use of such materials and to the extent that material may appear to be infringed, I assert that such alleged infringement is permissible under fair use principles in U.S. copyright laws. If you believe material has been used in an unauthorized manner, please contact the poster.

Supporters of President Donald Trump hold up Make America Great American and Keep America Great signs A supporter of Donald Trump dons a T-shirt with a new twist on an old joke targeting Hillary Clinton during a rally in Tampa, Florida on Tuesday, July 31, 2018. (Photo: Laura Baris/People’s Pundit Daily)

The Trump Campaign and Republican National Committee (RNC) joint fundraising efforts raised $105 million in the second quarter (Q2). A $54 million fundraising haul came from the campaign and committees, while the RNC raised $51 million.

Together, they boast a staggering $100 million cash on hand.

“Our massive fundraising success is a testament to the overwhelming support for President Trump,” said Brad Parscale, Campaign Manager for Donald J. Trump for President. “No Democrat candidate can match this level of enthusiasm or President Trump’s outstanding record of results.”

Donald J. Trump for President has $56 million cash-on-hand, while the RNC has $44 million.

“The RNC’s record-breaking fundraising has allowed us to identify troves of new supporters online and continue investing in our unprecedented field program,” said RNC Chairwoman Ronna McDaniel. “Our grassroots army is already hard at work–putting us in prime position to re-elect President Trump and Republicans across the country.”

President Trump packed the 20,000-capacity Amway Center in Orlando, Florida, to officially announce his campaign for a second term in June. He raised a record $24.5 million for his re-election campaign in less than 24 hours of his announcement in June.

For comparison, former vice president and Democratic frontrunner Joe Biden raised $6.3 million in the 24 hours after his campaign announcement. That amount is nearly as much as the campaign raised the entire first quarter (Q1) of 2019.

The campaign and committee are having similar fundraising success in the digital space. While doubling their digital investments from $31 million to $62 million, they raised more online in Q2 2019 than the first of 2018.

Q1 2019 Fundraising

The Trump Campaign raised more than $30 million for Q1 2019, a sizable haul exceeding all the top declared Democratic candidates, combined. The average donation to the campaign was just $34.26.

“Low-dollar” contributions are defined as $200 or less, and are indicative of grassroots enthusiasm and working-class support.

As People’s Pundit Daily (PPD) previously reported, roughly 98.5% of contributions to the Trump Campaign in Q4 2018 came from donations of $200 or less. In Q1 2019, that percentage ticked slightly higher to 98.79%.

The Q4 2019 total was nearly $10 million more than Q4 2018. The Trump Campaign had nearly 21 times more cash-on-hand than the Obama Campaign at that point in the re-election cycle.

On Liberty Never Sleeps, Tom laments the sad state of the world and how all of the crazy people are now running influential institutions of power.

The money pledged thru Patreon.com will go toward show costs such as advertising, server time, and broadcasting equipment. If we can get enough listeners, we will expand the show to two hours and hire additional staff.

To help our show out, please support us on Patreon.

All bumper music and sound clips are not owned by the show, are commentary, and of educational purposes, or de minimus effect, and not for monetary gain.

No copyright is claimed in any use of such materials and to the extent that material may appear to be infringed, I assert that such alleged infringement is permissible under fair use principles in U.S. copyright laws. If you believe material has been used in an unauthorized manner, please contact the poster.

American Manufacturing Sector Graphic Concept. (Photo: AdobeStock)

The Institute for Supply Management (ISM) Manufacturing Index (PMI) slowed 0.4 to 51.7%, slightly beating the consensus forecast at 51.1. Worth noting, the prices index declined and imports posted at zero expansion.

Indicator

Prior

Consensus Forecast

Forecast Range

Reading

ISM Manufacturing Index (PMI)

52.1

51.1

50.0 to 53.0

51.7

The New Orders Index came in at 50%, a decline of 2.7 percentage points from the May reading of 52.7%. The Production Index rose 2.8 percentage points to 54.1%.

The Employment Index continued to rise to 54.5%, a gain of 0.8 from the May reading of 53.7%. The Supplier Deliveries Index fell 1.3 to 50.7% from a reading of 52% in May. The Inventories Index registered 49.1%, a decrease of 1.8 percentage points from the May reading of 50.9%. The Prices Index registered 47.9%, a 5.3-percentage point decrease from the May reading of 53.2%.

“Comments from the panel reflect continued expanding business strength, but at soft levels,” Timothy R. Fiore, Chair of the ISM Manufacturing Business Survey Committee, said. “June was the third straight month with slowing PMI expansion.”

Capital Gains Investment Income Revenue Stock Market Ticker 3d Render Illustration. (Photo: AdobeStock)

One of the worst features of the internal revenue code is the pervasive bias against income that is saved and invested.

People who immediately consume their after-tax income are largely untaxed — thankfully, we don’t have a value-added tax — but there are several additional layers of tax on people who set aside income to finance future economic growth.

But that’s not a realistic option, so what about interim steps?

Interestingly, some progress may be possible. According to a Bloomberg report, the Trump Administration may be on the verge of getting rid of the hidden inflation tax on capital gains.

The White House is developing a plan to cut taxes by indexing capital gains to inflation, according to people familiar with the matter, in a move that…may be done in a way that bypasses Congress. Consensus is growing among White House officials to advance the proposal soon, the people said, to ensure the benefit takes effect before President Donald Trump faces re-election in 2020. Revamping capital gains taxes through a rule or executive order likely would face legal challenges, a concern that reportedly prompted former President George H.W. Bush’s administration to drop a similar plan. …Indexing capital gains would slash tax bills for investors when selling assets such as stock or real estate by adjusting the original purchase price so no tax is paid on appreciation tied to inflation. …The inflation adjustment would amount to a several percentage point tax cut for investors, depending on the type of asset and how long it’s held, according to 2018 estimates from the non-partisan Congressional Research Service. Corporate stock with dividends held for 10 years would be currently be subject to an effective tax rate of 24.3%. That same holding indexed to inflation would be subject to a 21.4% tax rate, CRS said.

Kimberley Strassel of the Wall Street Journalopines that this would be a very desirable reform.

What if President Trump had the authority—on his own—to enact a second powerful tax reform? He does. The momentum is building for him to use it. …forces are aligning behind a plan: a White House order to index capital gains for inflation. It’s a long-overdue move—one that would further unleash the economy and boost GOP election prospects. …At President Reagan’s behest, Congress in the 1980s indexed much of the federal tax code for inflation. Oddly, capital gains weren’t similarly treated. The result is that businesses and individuals pay taxes on the full nominal amount they earn on investments, even though inflation eats up a good chunk of any gain. It’s not unheard of for taxes to exceed real gains after inflation. …the Internal Revenue Code does not require that the “cost” of an asset be measured only as its original price—meaning there is no reason Treasury could not construe it in today’s dollars. …The move would set off an explosion of buying and selling—of which the government would get its cut. The lower tax on capital would also help asset prices grow. All of this would be excellent news for the economy.

This 2010 video from the Center for Freedom and Prosperity elaborates on the reasons for indexing.

I especially like the examples showing how, even with modest levels of inflation, the actual capital gains tax rate can be much higher than official rate.

Remember, it’s the effective marginal tax rate that determines incentives for additional productive activity.

This is why any form of capital gains taxation is wrong. And it’s especially wrong to impose a hidden – and higher – tax simply because of inflation. Indeed, it is fundamentally immoral to let the government profit from inflation.

So, what would happen if the rumors are true and Trump unilaterally eliminates the tax on inflationary gains?

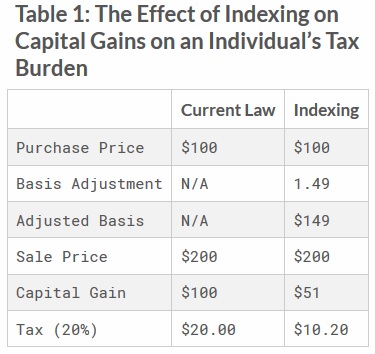

The Tax Foundation estimated how such a change would affect the economy and the budget. The report includes a helpful example of how this reform would protect investors.

…if an individual purchased an asset for $100 in January 1, 2000 and sold that asset for $200 on July 1, 2018, the nominal capital gain would be $100. However, inflation over that period increased the price level by 49 percent. Under an indexing proposal, the individual would be able to gross up the basis of $100 by the total inflation during that period to $149. As a result, the individual would only be taxed on $51 instead of the full $100.

Here’s a table comparing the status quo with indexing.

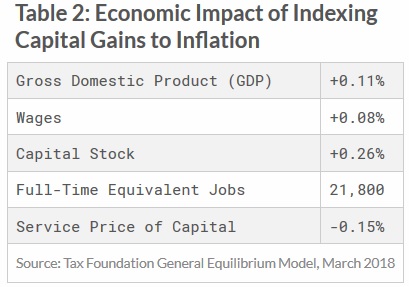

Here’s the estimate of the economic benefits.

…indexing capital gains to inflation would increase the long-run size of the economy by 0.11 percent, which is equivalent to about $22 billion in 2018. This provision would primarily boost output by reducing the service price of capital, which would increase the incentive to invest in the United States. We estimate that the service price of capital would be 0.15 percent lower under this proposal. The capital stock would be 0.26 percent larger and the larger capital stock would boost labor productivity leading to 0.08 percent higher wages.

And here’s the accompanying table.

The Tax Foundation also prepared an estimate of the impact on tax revenue.

On a dynamic basis, the revenue loss would be…$148.3 billion over the next ten years. The increase in output due to the lower cost of capital would boost incomes, which would boost payroll revenue and slightly offset individual income tax revenue losses.

The bottom line is that this is not a self-financing reform, but it is a reform that would help the economy by encouraging more jobs and growth.

And, remember, even small improvements in growth have a meaningful impact over time.

Let’s close with a video from an unlikely supporter of inflation indexing.

Notwithstanding these remarks, I don’t think Schumer will applaud if Trump indexes the capital gains tax. Instead, I suspect he’s now more likely to support measures that would exacerbate this form of double taxation.

Though I think he’s still on the right side (at least behind the scenes) on the issue of “carried interest,” so maybe he’s not a totally lost cause.

The month of July will mark the longest U.S. expansion since the mid-1850s, surpassing the prior 10-year record from March 1991 to March 2001. In June, the current expansion beginning after the Great Recession ended in June 2009 tied the prior 120-month record, and July will make 121 months.

On September 20, 2010, the Business Cycle Dating Committee of the National Bureau of Economic Research (NBER) announced that a trough in business activity occurred in the U.S. economy in June 2009.

It signaled the end of the Great Recession that began in December 2007 and the beginning of an expansion. The recession lasted 18 months, making it the longest of any since World War II.

The longest postwar recessions prior each lasted 16 months, one from November 1973 to March 1975 and the other July 1981 to November 1982.

U.S. economy on an American flag background waving in the wind, in 3D rendering. (Photo: AdobeStock)

Last week, the Bureau of Economic Analysis (BEA) reported the third estimate for first quarter (Q1) 2019 gross domestic product (GDP) showed the U.S. economy grew at a solid annual rate of 3.1%. In Q4 2018, the U.S. economy as measured by real GDP rose 2.2%.

Contractions (recessions) start at the peak of a business cycle and end at the trough. Durations below are in months.

You have %%pigeonMeterAvailable%% free %%pigeonCopyPage%% remaining this month. Get unlimited access and support reader-funded, independent data journalism.